Introduction

Underwriting commercial real estate is the cornerstone of disciplined commercial real estate investing, lending, and development. Whether you are a commercial real estate investor, a lender evaluating a commercial loan, a developer preparing an acquisition, an asset manager overseeing cash flow, or a broker packaging a deal, understanding how underwriting commercial real estate works will help you evaluate property value, estimate loan amount feasibility, and make informed decisions about risk and return. This guide explains what underwriting commercial real estate underwriting is, why it matters, and the commercial real estate underwriting process step by step.

What Is Underwriting Commercial Real Estate?

Underwriting commercial real estate is the process through which an underwriter analyzes a commercial property to approve or deny the loan, determine loan terms, and size the loan amount relative to property value and projected cash flow. Underwriting in commercial real estate focuses on assessing net operating income (NOI), debt service coverage ratio (DSCR), market conditions, tenant quality, vacancy rate, operating expenses, and the overall viability of a commercial real estate investment. CRE underwriting combines financial modeling, property appraisal, commercial property risk assessment, and legal and technical due diligence to establish whether a borrower will be able to repay the loan and whether the property supports the proposed loan underwriting models.

Why Underwriting Commercial Real Estate Matters

Effective underwriting commercial real estate protects lenders from default, helps investors understand cash flow and value, guides developers on financing feasibility, and enables brokers to price and present deals accurately. It directly affects loan underwriting decisions, including loan terms, interest rates, loan-to-value (LTV) limits, and required covenants. A thorough commercial real estate underwriting process reduces surprises, unexpected operating expenses, inaccurate NOI, tenant turnover, or market shifts, and increases the likelihood that loan payments will be made on time and the real estate investment meets return expectations.

Key Components of the Commercial Real Estate Underwriting Process

The commercial real estate underwriting process typically follows a structured set of analyses. Below are the core components every real estate underwriter covers when underwriting commercial real estate:

1. Financial Modeling and Net Operating Income (NOI) Analysis

Financial modeling is central to underwriting commercial real estate. Underwriting models start with projected gross potential income, subtract vacancy and credit loss to arrive at adequate gross income, then deduct operating expenses to determine net operating income. NOI is pivotal because it determines the property’s ability to service debt. Lenders evaluate NOI against projected debt service to calculate DSCR. With NOI and an acceptable DSCR, a lender can estimate a sustainable commercial loan amount. Underwriting focuses on realistic revenue forecasts from leases, rent escalations, ancillary income, and conservative vacancy assumptions.

2. Debt Service Coverage Ratio (DSCR) and Loan Sizing

DSCR analysis compares net operating income to expected debt service (loan payments). For example, a lender may require a minimum DSCR of 1.25x for a commercial loan, meaning NOI must be 25% higher than annual debt service. Underwriting commercial real estate consistently models multiple interest rate and amortization scenarios to see how changes in interest rates, loan terms, or operating expenses affect DSCR and the ability to repay the loan. The DSCR drives loan sizing and, combined with LTV, determines the loan amount the lender is comfortable offering.

3. Cap Rate and Value of the Property

Cap rate is a standard valuation metric for commercial properties: property value equals NOI divided by cap rate. Underwriting commercial real estate involves reconciling market-derived cap rates with the subject property’s NOI. Appraisals will use recent sales, income capitalization, and cost approaches to confirm the value of the property. The result affects LTV calculations and the loan underwriting decision.

4. Market Conditions and Commercial Property Risk Assessment

Underwriting in commercial real estate requires careful assessment of market conditions: supply and demand, new construction pipelines, employment trends, interest rates, and local economic drivers. A commercial real estate underwriter evaluates vacancy rates, rent trends, and comparable property performance to determine whether the market supports the income assumptions in the underwriting models. This commercial property risk assessment helps identify systemic risks that could affect the property’s cash flow and property underwriting conclusions.

5. Tenant and Lease Analysis

For income-producing commercial properties, leases and tenant quality are critical. Underwriting commercial real estate involves assessing lease terms, rent rolls, lease expirations, tenant creditworthiness, and rent diversification. Long-term, creditworthy tenants reduce vacancy risk and stabilize cash flow. Underwriting also examines lease structures, triple net (NNN), gross, or modified gross, to allocate operating expense responsibility between tenant and landlord, as these affect NOI and operating expenses assumptions.

6. Operating Expenses and Property Management

Operating expenses impact net operating income and long-term cash flow. Underwriting commercial real estate includes a line-by-line review of property taxes, insurance, utilities, repairs and maintenance, property management fees, and capital reserves. Adequate property management and prudent reserves for capex reduce the probability of sudden spikes in expenses that can jeopardize debt service and overall investment returns.

7. Legal, Environmental, and Physical Due Diligence

Underwriting commercial real estate is incomplete without legal, environmental, and physical inspections. Title reviews, survey checks, zoning compliance, environmental site assessments, and property condition assessments feed into the overall risk profile and may influence loan terms or require escrows. Undetected legal or ecological problems can dramatically reduce the value of the property and increase lender exposure.

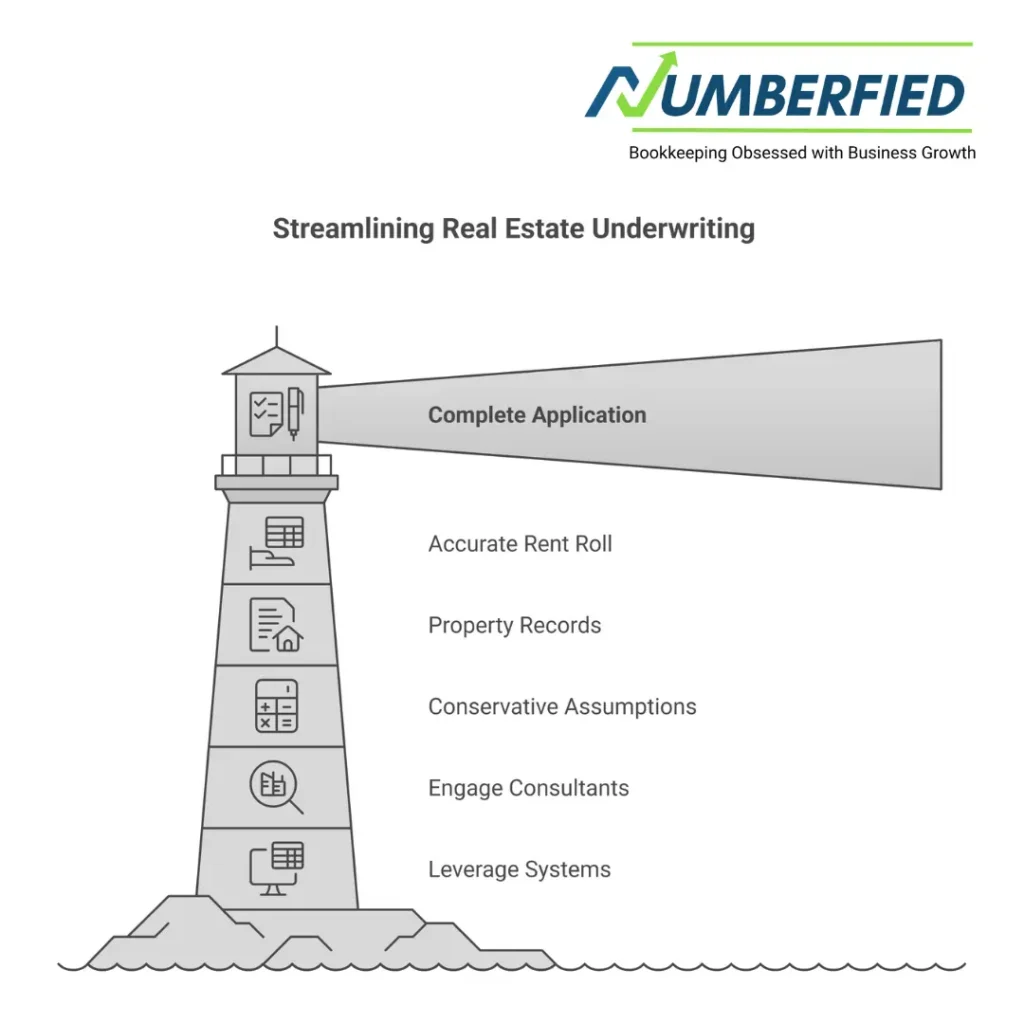

Step-by-Step Underwriting Commercial Real Estate

Below is a practical step-by-step workflow that lenders, investors, and underwriters follow when underwriting commercial real estate:

Step 1: Initial Screening and Loan Application Review

Receive the loan application, executive summary, rent roll, financial statements, broker package, and property-level documents. Perform a preliminary check for property type, location, loan amount requested, LTV targets, and whether the transaction fits the lender’s or investor’s underwriting criteria.

Step 2: Financial Analysis and Underwriting Models

Build the underwriting models: project gross income, vacancy, NOI, operating expenses, and cash flow. Run base, stress, and upside scenarios to test DSCR sensitivity to rent downturns or increased vacancy. Estimate the cap rate-derived value and reconcile with the appraisal and comparable sales.

Step 3: Market and Tenant Due Diligence

Research market conditions, vacancy rates, employment trends, and comparable lease rates. Analyze the rent roll, verify tenant financials, and assess concentration risk from large tenants with looming lease expirations. Confirm demand drivers for the property type and submarket.

Step 4: Technical and Legal Review

Order property appraisal, environmental site assessment, property condition assessment, title report, and zoning verification. Review leases, estoppel certificates, and service contracts. Identify any legal covenants, liens, or environmental issues that could influence underwriting decisions.

Step 5: Final Underwriting and Loan Structuring

Finalize the underwriting commercial real estate memo with recommended loan amount, LTV, interest rate, amortization, covenants, reserves, and required insurance. Include contingencies based on appraisal value, environmental clean-up, or capex allowances. Prepare the loan commitment with clear loan terms and closing conditions.

Step 6: Approval, Closing, and Post-Closing Monitoring

Underwriting commercial real estate culminates in approving or denying the loan. Once approved, close with the borrower and implement post-closing monitoring for financial statements, rent collection, and compliance with loan covenants. Ongoing monitoring protects the lender and supports asset management.

Financial Modeling Best Practices

When underwriting commercial real estate, financial modeling should be conservative, transparent, and flexible. Key best practices include:

- Use conservative vacancy rates and market-driven rent growth assumptions.

- Model multiple interest rate scenarios to understand sensitivity to interest rate increases.

- Include realistic operating expenses, property tax adjustments, and capital expenditure reserves.

- Calculate NOI, DSCR, and cash flow to equity under both current and stressed scenarios.

- Reconcile the cap rates used in valuation with market transactions and appraisal results.

Residential vs. Commercial Underwriting Differences

Underwriting commercial real estate differs from residential underwriting in several ways. Commercial underwriting focuses on the property’s income-producing ability (NOI) and tenant quality, whereas residential underwriting emphasizes borrower credit, employment, and personal income. Commercial loan underwriting often relies on property-level cash flow to repay the loan, leading to more complex lease analysis, greater sensitivity to vacancy and market cycles, and diverse property types that require specialized market knowledge. Lenders use different underwriting models, loan terms, and risk tolerances for commercial properties compared to single-family residential loans.

In-House vs. Outsourced Underwriting

Organizations choose between in-house underwriting and outsourced underwriting based on capacity, expertise, and speed requirements. In-house underwriting gives lenders and asset managers direct control, consistent underwriting standards, and closer integration with origination teams. Outsourced underwriting can scale quickly, provide specialized expertise for uncommon property types, and reduce overhead. Whether in-house or outsourced, automated underwriting systems and standardized underwriting models help maintain consistency and speed while ensuring commercial real estate underwriting focuses on core risks.

Common Mistakes in Underwriting Commercial Real Estate

Common errors to avoid when underwriting commercial real estate include:

- Overstating rental income or underestimating vacancy rate and operating expenses.

- Using an optimistic cap rate or failing to reconcile the value of the property with market comps.

- Ignoring lease expiration schedules and tenant concentration risk.

- Underestimating future capital expenditures and deferred maintenance identified in the property condition assessment.

- Neglecting local market conditions and economic drivers that influence demand.

Tools and Software for Faster, More Accurate Underwriting

Modern underwriting leverages tools that speed the commercial real estate underwriting process while improving accuracy. Standard tools include commercial loan origination systems, underwriting models in Excel with scenario engines, automated underwriting systems for preliminary credit checks, property appraisal management platforms, and lease abstraction software to analyze leases quickly. Data providers and market intelligence platforms supply vacancy, cap rate, and rent trend data. Using these tools helps underwriters evaluate property underwriting models, run NOI and DSCR analysis faster, and assemble a complete loan application package for quicker approvals.

Practical Tips for Faster Approvals and Stronger Underwriting

To streamline the commercial real estate underwriting process and improve approval odds:

- Prepare a complete loan application with a clear executive summary, rent roll, tenant financials, and supporting documents.

- Provide an accurate, up-to-date rent roll and lease abstracts to speed tenant analysis.

- Supply recent property tax records, insurance certificates, and property condition reports to reduce due diligence delays.

- Use conservative underwriting assumptions for NOI, vacancy, and operating expenses.

- Engage a reputable appraiser and environmental consultant early to avoid surprises in the underwriting process.

- Leverage underwriting templates and automated underwriting systems to ensure consistency and speed.

How Underwriting Commercial Real Estate Helps Make Informed Decisions

Underwriting commercial real estate equips commercial real estate investors, lenders, and developers with the quantitative and qualitative analysis needed to make informed decisions. Thorough underwriting illuminates cash flow projections, evaluates the property’s ability to repay the loan, quantifies downside scenarios, and identifies remediation steps for risk mitigation. Whether you are considering commercial real estate investment opportunities, preparing a commercial loan application, or deciding whether to acquire a commercial property, a robust underwriting process establishes the facts and assumptions that support a sound decision.

Practical Example: Underwriting a Mid-Size Office Building

Consider underwriting a 50,000-square-foot office building with a current NOI of $450,000, a market cap rate of 6.0%, and a lender-required DSCR of 1.3x. Using the cap rate, the property’s value would be approximately $7.5 million (NOI / cap rate). If the lender permits an LTV of 70%, the preliminary loan amount could be about $5.25 million. Underwriting commercial real estate using models: annual debt service at the proposed interest rate and amortization, then checks DSCR. If yearly debt service is $350,000, DSCR = 450,000 / 350,000 = 1.29x, slightly below the 1.3x requirement. The underwriter can adjust loan terms larger down payment, longer amortization, or a higher interest rate cushion, or require additional covenants or reserves to achieve the required DSCR and approve the commercial loan.

Final Checklist for Successful Underwriting Commercial Real Estate

Use this checklist to ensure a comprehensive underwriting in commercial real estate:

- Complete loan application and executive summary

- Up-to-date rent roll and lease abstracts

- Detailed financial model with NOI, DSCR, cash flow, and sensitivity analysis

- Market research showing comparable rents, vacancy rates, and cap rates

- Appraisal, environmental site assessment, and property condition report

- Title report, survey, and zoning verification

- Clear recommendation on loan amount, LTV, interest rate, amortization, and covenants

Conclusion

Underwriting commercial real estate is a disciplined, multi-faceted process that blends financial modeling, market research, lease and tenant analysis, property condition and legal due diligence, and risk assessment. Whether you are a commercial real estate investor evaluating property investment, a lender performing commercial loan underwriting, a developer planning a real estate acquisition, an asset manager optimizing cash flow and property management, or a broker preparing a deal package, mastering underwriting commercial real estate improves decision-making, reduces risk, and speeds approvals.

If you want to improve your underwriting models, validate a loan application, or assess the viability of a commercial real estate investment, request a free consultation with our underwriting experts. We provide tailored commercial real estate underwriting support, detailed NOI and DSCR analysis, market and tenant assessments, and clear loan structuring recommendations to help you close deals with confidence.

Request your free consultation today and get expert help with underwriting commercial real estate to evaluate real estate opportunities, optimize loan terms, and make informed decisions.

FAQ

What do commercial underwriters do?

Commercial underwriters evaluate the risk of loans secured by income-producing properties such as offices, retail centers, apartments, or industrial buildings. They analyze property cash flow, occupancy rates, debt service coverage ratio, borrower financials, market conditions, and property condition to determine if the loan is safe for the lender. Their work ensures the property generates enough income to repay the loan and protects the lender from potential default.

What are the 4 types of underwriting?

The four main types of underwriting are residential underwriting (for homes and small multifamily), commercial underwriting (for income-producing properties), construction underwriting (for new development or major renovations), and bridge underwriting (for short-term transitional loans). Each type has different risk profiles, documentation requirements, and focus areas based on the property and loan purpose.

What is underwriting in commercial real estate?

Underwriting in commercial real estate is the detailed risk assessment process where the lender reviews the property’s income potential, borrower’s financial strength, market conditions, and property condition to approve or deny a loan. It focuses heavily on cash flow (NOI), debt service coverage, loan-to-value ratio, and tenant quality to ensure the property can support the debt.

What are the three types of underwriting?

The three primary types of underwriting are residential (personal borrower-focused), commercial (property income-focused), and construction/bridge (project or transitional-focused). Commercial underwriting emphasizes cash flow and property performance, while residential prioritizes borrower credit and income, and construction/bridge assesses development risk and exit strategy.

How does underwriting work in real estate?

Underwriting in real estate involves reviewing the borrower’s credit, income, assets, debt obligations, and the property’s appraisal, title, and market conditions. The underwriter verifies all documents, calculates key ratios (LTV, DSCR, DTI), identifies risks, and decides whether to approve the loan, require conditions, or deny it based on lender guidelines and risk tolerance.

How does commercial underwriting work?

Commercial underwriting focuses on the property’s ability to generate income to repay the loan. The underwriter analyzes net operating income, occupancy history, tenant leases, market rents, expense ratios, and debt service coverage. They also review the borrower’s financials, credit, and experience, then approve, condition, or deny based on risk and lender standards.

Can you get denied during underwriting?

Yes, loans are frequently denied during underwriting, even after pre-approval. Common reasons include low appraisal, insufficient income or cash flow, high debt-to-income ratio, poor credit updates, title issues, environmental concerns, or non-compliance with lender guidelines. Underwriting is the final risk review stage before closing.

What are the 3 C’s of underwriting?

The three C’s of underwriting are Credit (borrower’s credit history and score), Capacity (ability to repay based on income and debt obligations), and Collateral (property value and condition as security for the loan). These core principles help underwriters assess overall risk and determine loan approval.

What are common underwriting mistakes?

Common underwriting mistakes include overlooking declining property cash flow, accepting unverifiable income sources, missing title or lien issues, underestimating market risks, failing to account for deferred maintenance, ignoring borrower credit changes, or miscalculating the debt service coverage ratio. These errors can lead to loan defaults or unnecessary denials.

Read Also: Virtual Bookkeeping Services for Small Businesses That’ll Change Your Life!