Introduction

In the dynamic world of property investments, commercial real estate underwriting stands as a cornerstone process that ensures sound financial decisions. This critical evaluation helps lenders assess the viability of loans for office buildings, retail spaces, and industrial properties, protecting both parties from potential pitfalls. We understand the complexities involved, and through this guide, we aim to provide you with valuable knowledge to navigate this landscape effectively. Whether you are an investor seeking funding or a lender evaluating opportunities, grasping commercial real estate underwriting can lead to more successful outcomes. By delving into its principles, you will gain the tools needed to mitigate risks and capitalize on market potential.

Key Takeaways

- Commercial real estate underwriting involves a thorough analysis of financial, market, and property-specific factors to determine loan feasibility.

- Effective underwriting reduces investment risks by identifying potential issues early in the process.

- Understanding key metrics like debt service coverage ratio and loan-to-value ratio is essential for all stakeholders.

- Staying informed about regulatory changes and economic trends enhances underwriting accuracy.

- Collaboration between borrowers and lenders fosters transparent and efficient underwriting experiences.

What is Commercial Real Estate Underwriting?

Commercial real estate underwriting refers to the detailed examination conducted by lenders to evaluate the risks and rewards associated with financing commercial properties. This process goes beyond simple credit checks, incorporating a holistic view of the asset’s potential performance.

Definition and Core Components

At its core, commercial real estate underwriting entails reviewing financial statements, property appraisals, and market data to ascertain if a loan aligns with the lender’s criteria. Lenders scrutinize income projections, expense forecasts, and cash flow stability to build a comprehensive picture. This step ensures that the property can generate sufficient revenue to cover debt obligations over time.

Importance in the Financing Landscape

The significance of commercial real estate underwriting cannot be overstated, as it safeguards investments against unforeseen economic shifts. Identifying strengths and weaknesses early allows for adjustments that enhance project viability. Ultimately, robust underwriting contributes to a healthier real estate market by promoting responsible lending practices.

Key Players Involved

Various professionals play pivotal roles in commercial real estate underwriting, including underwriters, appraisers, and financial analysts. Underwriters lead the evaluation, coordinating inputs from appraisers who assess property values based on comparable sales and income approaches. Financial analysts provide insights into borrower qualifications, ensuring a collaborative effort that yields reliable results.

The Step-by-Step Process of Commercial Real Estate Underwriting

Navigating commercial real estate underwriting requires a structured approach, broken down into sequential stages that build upon each other. This methodical process helps in uncovering all relevant details systematically.

Initial Application Review

The journey begins with an initial review of the loan application, where basic information such as property details and borrower background is examined. Lenders verify documentation for completeness and accuracy, setting the foundation for deeper analysis. This phase often includes preliminary credit checks to gauge initial eligibility.

In-Depth Financial Analysis

Following the initial review, a thorough financial analysis takes center stage in commercial real estate underwriting. This involves dissecting income statements, balance sheets, and cash flow projections to evaluate the property’s earning potential. Metrics like net operating income are calculated to determine if the asset can support the proposed debt.

Property and Market Evaluation

An essential component is the evaluation of the property itself and prevailing market conditions. Appraisals are conducted to establish fair market value, while market studies assess demand, vacancy rates, and competitive landscapes. This step ensures that external factors are factored into the underwriting decision.

Risk Assessment and Mitigation Strategies

Risk assessment forms a critical part of commercial real estate underwriting, identifying potential threats such as tenant turnover or interest rate fluctuations. Strategies are then developed to mitigate these risks, including requiring additional collateral or adjusting loan terms. This proactive approach enhances the overall security of the financing arrangement.

Final Decision and Documentation

The process culminates in a final decision, where all findings are synthesized to approve, deny, or modify the loan request. Approved loans proceed to documentation, outlining terms and conditions clearly. This stage emphasizes transparency to build trust between lenders and borrowers.

Key Factors Influencing Commercial Real Estate Underwriting

Several factors profoundly impact the outcomes of commercial real estate underwriting, requiring careful consideration to achieve balanced assessments.

Property Valuation Techniques

Accurate property valuation is fundamental in commercial real estate underwriting, employing methods like the cost approach, sales comparison, and income capitalization. The income approach, particularly relevant for income-producing properties, projects future cash flows discounted to present value. These techniques provide a solid basis for determining loan amounts.

Borrower Creditworthiness Assessment

Evaluating the borrower’s creditworthiness is a key pillar of commercial real estate underwriting. This includes reviewing credit history, debt-to-income ratios, and financial stability. Strong credit profiles can lead to more favorable loan terms, reflecting the borrower’s ability to manage obligations effectively.

Market and Economic Conditions

Market and economic conditions heavily influence commercial real estate underwriting decisions. Factors such as employment rates, consumer spending, and interest rate trends are analyzed to predict property performance. In booming markets, underwriting may be more lenient, while recessions prompt stricter scrutiny.

Environmental and Legal Considerations

Environmental assessments and legal reviews are integral to commercial real estate underwriting, ensuring compliance with regulations. Phase I environmental site assessments identify potential hazards, while title searches confirm clear ownership. Addressing these early prevents costly issues down the line.

Tenant and Lease Analysis

For leased properties, tenant and lease analysis is crucial in commercial real estate underwriting. Reviewing lease terms, tenant credit, and occupancy rates helps forecast reliable income streams. Strong, long-term leases bolster the underwriting case by demonstrating stable revenue potential.

Common Challenges in Commercial Real Estate Underwriting

Despite its structured nature, commercial real estate underwriting presents several challenges that require adept handling.

Dealing with Economic Volatility

Economic volatility poses a significant challenge in commercial real estate underwriting, as sudden shifts can alter property values and income projections. Underwriters must incorporate stress testing to simulate adverse scenarios, ensuring resilience. This foresight helps in crafting loans that withstand economic downturns.

Navigating Regulatory Changes

Regulatory changes frequently impact commercial real estate underwriting, with new laws affecting lending standards and compliance requirements. Staying abreast of updates from bodies like the FDIC is essential for accurate assessments. Adapting to these changes maintains the integrity of the underwriting process.

Ensuring Data Accuracy and Completeness

Data accuracy is a perennial challenge in commercial real estate underwriting, where incomplete or erroneous information can skew evaluations. Implementing rigorous verification protocols and cross-checking sources mitigates this risk. Accurate data forms the bedrock of trustworthy underwriting outcomes.

Addressing Property-Specific Risks

Property-specific risks, such as structural issues or location disadvantages, complicate commercial real estate underwriting. Detailed inspections and site visits reveal these concerns, allowing for appropriate adjustments. Proactive identification ensures that risks are managed effectively.

Managing Borrower Expectations

Balancing borrower expectations with realistic underwriting outcomes is another hurdle. Clear communication throughout the process helps align perspectives and reduce frustrations. This approach fosters positive relationships and smoother transactions.

Best Practices for Effective Commercial Real Estate Underwriting

Adopting best practices elevates the quality of commercial real estate underwriting, leading to better-informed decisions.

Conducting Thorough Due Diligence

Thorough due diligence is paramount in commercial real estate underwriting, encompassing comprehensive reviews of all relevant documents and data. This includes verifying financials, legal titles, and environmental reports meticulously. Such diligence uncovers hidden issues, enhancing decision-making confidence.

Leveraging Technology and Tools

Technology plays a transformative role in commercial real estate underwriting, with software streamlining data analysis and modeling. Tools like automated valuation models accelerate appraisals, while data analytics provide deeper insights. Embracing these innovations improves efficiency and accuracy.

Fostering Collaboration Among Stakeholders

Collaboration among stakeholders is a best practice that enriches commercial real estate underwriting. Regular communication between lenders, borrowers, and appraisers ensures all viewpoints are considered. This teamwork leads to more holistic evaluations and mutually beneficial outcomes.

Continuous Education and Training

Ongoing education keeps underwriters sharp in the evolving field of commercial real estate underwriting. Training programs on new regulations and market trends maintain high standards. Investing in professional development sustains expertise and adaptability.

Implementing Robust Risk Management Frameworks

Robust risk management frameworks are essential for successful commercial real estate underwriting. These include standardized procedures for risk identification and mitigation. Consistent application of these frameworks minimizes exposure and supports sustainable lending.

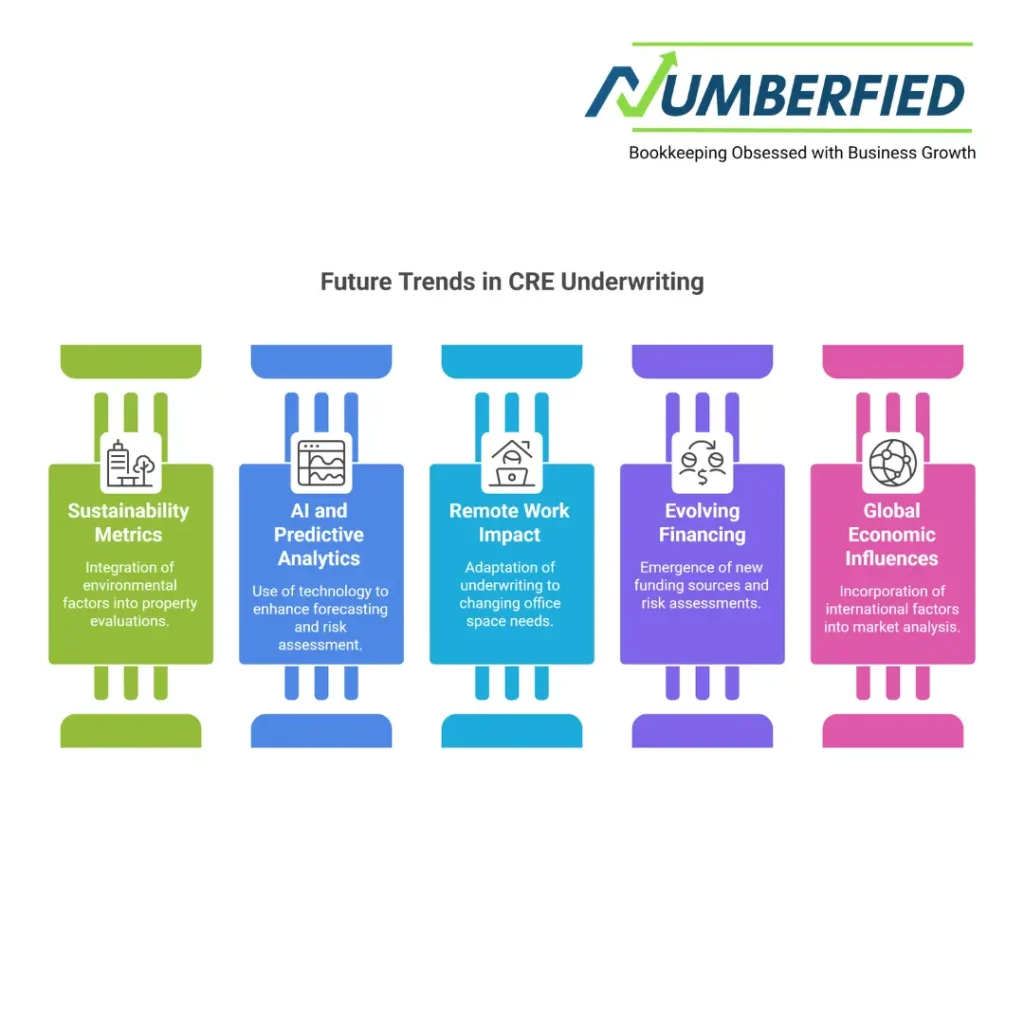

Future Trends Shaping Commercial Real Estate Underwriting

Looking ahead, several trends are poised to redefine commercial real estate underwriting, offering new opportunities and considerations.

Integration of Sustainability Metrics

Sustainability is increasingly integrated into commercial real estate underwriting, with lenders evaluating energy efficiency and green certifications. Properties meeting ESG criteria may secure better terms, reflecting growing environmental awareness. This trend promotes responsible development and long-term value.

Adoption of AI and Predictive Analytics

AI and predictive analytics are revolutionizing commercial real estate underwriting by enhancing forecasting accuracy. Machine learning algorithms analyze vast datasets to predict market behaviors and risks. These tools enable faster, more precise evaluations, transforming traditional processes.

Impact of Remote Work on Property Assessments

The rise of remote work influences commercial real estate underwriting, particularly for office spaces. Underwriters now assess adaptability for hybrid models and potential repurposing. This shift requires updated valuation methods to account for changing occupancy patterns.

Evolving Financing Structures

Innovative financing structures, such as crowdfunding and alternative lenders, are emerging in commercial real estate underwriting. These options expand access but necessitate adapted risk assessments. Understanding these structures ensures comprehensive underwriting in a diversifying market.

Global Economic Influences

Global economic influences are becoming more pronounced in commercial real estate underwriting, with international trade and geopolitics affecting local markets. Underwriters must incorporate broader perspectives to anticipate impacts. This global view strengthens resilience against external shocks.

Case Studies in Commercial Real Estate Underwriting

Real-world examples illustrate the application of commercial real estate underwriting principles, providing practical insights.

Successful Retail Property Financing

In one case, commercial real estate underwriting for a retail center involved detailed tenant analysis and market forecasting, leading to a favorable loan. The process highlighted strong lease agreements, resulting in low-risk approval. This example demonstrates the value of comprehensive evaluations.

Overcoming Challenges in Industrial Lending

An industrial property faced underwriting hurdles due to environmental concerns, but thorough assessments resolved issues. Adjustments to loan terms mitigated risks, enabling financing. This case underscores the importance of proactive problem-solving.

Office Space Adaptation Post-Pandemic

Post-pandemic underwriting for an office building incorporated remote work trends, adjusting valuations accordingly. Innovative lease structures were evaluated, securing funding. This illustrates adaptability in evolving markets.

Multifamily Housing Project Evaluation

Commercial real estate underwriting for a multifamily project focused on occupancy projections and economic indicators. Positive findings supported approval, highlighting demographic trends. The case shows how data-driven decisions drive success.

Mixed-Use Development Insights

A mixed-use development’s underwriting revealed synergies between components, enhancing overall viability. Integrated analysis led to optimized financing. This example emphasizes holistic approaches.

Conclusion

In summary, commercial real estate underwriting serves as a vital mechanism for ensuring prudent investments in the property sector. By understanding its processes, key factors, challenges, and best practices, you can approach financing with greater confidence and foresight. We have explored how this evaluation safeguards against risks while unlocking opportunities, emphasizing the need for thorough analysis and adaptation to trends. As you apply these insights, remember that effective commercial real estate underwriting paves the way for sustainable growth. We invite you to reach out to Numberfied for personalized guidance on your real estate endeavors. Contact us today to discuss how we can support your goals.

FAQs

What role does cash flow analysis play in commercial real estate underwriting?

Cash flow analysis is central to assessing a property’s ability to generate income sufficient for debt repayment. It involves projecting revenues minus expenses to calculate net operating income. This metric helps lenders determine if the investment is viable long-term.

How do interest rates affect commercial real estate underwriting outcomes?

Interest rates influence borrowing costs and property valuations, impacting affordability assessments. Higher rates may tighten underwriting criteria to ensure coverage ratios remain strong. Lenders adjust terms to balance risks in fluctuating rate environments.

Why is location analysis crucial in commercial real estate underwriting?

Location affects demand, accessibility, and growth potential, directly influencing property performance. Underwriters evaluate demographics, infrastructure, and zoning to predict success. A prime location can strengthen the case for loan approval.

What documentation is typically required for commercial real estate underwriting?

Required documents include financial statements, tax returns, appraisals, and lease agreements. These provide evidence of income stability and asset value. Complete submissions expedite the review process.

How does the debt service coverage ratio factor into commercial real estate underwriting?

The debt service coverage ratio measures income available to cover debt payments, ideally above 1.25. It ensures the property can handle obligations comfortably. Lower ratios may lead to loan denials or modifications.

In what ways can borrowers prepare for commercial real estate underwriting?

Borrowers should organize financial records, conduct preliminary appraisals, and address potential issues upfront. Understanding lender requirements streamlines the process. Preparation demonstrates reliability and can improve approval chances.

What impact do zoning laws have on commercial real estate underwriting?

Zoning laws dictate permissible uses, affecting development potential and value. Underwriters verify compliance to avoid legal risks. Non-conforming properties may require variances, complicating evaluations.

How is the loan-to-value ratio used in commercial real estate underwriting?

The loan-to-value ratio compares the loan amount to the property value, typically capped at 70-80%. It assesses equity and risk exposure. Lower ratios indicate safer investments for lenders.

Why consider historical performance in commercial real estate underwriting?

Historical data reveals trends in occupancy, revenue, and expenses, informing future projections. It helps identify patterns and risks. Reliable history supports stronger underwriting cases.

How do alternative data sources enhance commercial real estate underwriting?

Alternative sources like satellite imagery or consumer behavior data provide additional insights. They complement traditional metrics for more accurate assessments. This approach improves risk prediction and decision quality.

Read Also: Virtual Bookkeeping Services for Small Businesses That’ll Change Your Life!