Introduction

We are pleased to present a clear and structured approach to how to underwrite a real estate deal, one of the most valuable skills for real estate investors throughout the United States. Proper underwriting allows you to assess whether a property will generate the returns you expect while protecting you from unnecessary financial exposure. In an ever-changing market influenced by interest rates, local economics, and property-specific factors, knowing how to underwrite a real estate deal provides the clarity needed to move forward confidently or walk away from unfavorable opportunities.

Key Takeaways

- Underwriting combines quantitative financial review with qualitative market and property evaluation.

- The process helps determine true value, projected cash flow, and overall investment risk.

- Accurate underwriting supports better negotiation, financing approval, and long-term portfolio performance.

- Use reliable data sources and conservative assumptions to build trustworthy models.

- Regular practice with real deals improves speed and precision over time.

Understanding the Fundamentals of Real Estate Underwriting

What Does It Mean to Underwrite a Real Estate Deal?

Underwriting is the detailed examination of a property’s financials, market position, and risks to decide if it represents a sound investment. The goal is to project future performance with reasonable accuracy. When you learn how to underwrite a real estate deal, you gain the ability to separate promising opportunities from those that appear attractive only on the surface.

Why Underwriting Matters for Every Investor

Skipping or rushing underwriting frequently leads to overpaying, unexpected expenses, or cash-flow shortfalls. Thorough analysis protects capital and increases the probability of achieving targeted returns. We view underwriting as the foundation of disciplined real estate investing across residential, multifamily, and commercial asset classes.

Who Participates in the Underwriting Process?

Investors lead the effort, but lenders, appraisers, property managers, inspectors, and attorneys often provide critical input. Each participant contributes specialized knowledge that strengthens the overall evaluation. Coordination among these parties is essential for a complete picture when determining how to underwrite a real estate deal.

Common Myths About the Underwriting Process

Some assume underwriting applies only to large commercial transactions, yet even single-family rentals benefit greatly from structured analysis. Others believe it is purely mathematical; in reality, judgment about location quality and tenant stability plays an equally important role.

Preparing for Effective Underwriting

Collecting and Organizing Financial Records

Request current rent rolls, trailing twelve-month profit-and-loss statements, utility bills, and insurance policies. Secure copies of existing leases and service contracts as well. Organized records allow you to verify seller-provided numbers quickly and accurately.

Researching Local Market Conditions

Study recent comparable sales, current rental listings, and vacancy statistics in the immediate submarket. Review demographic trends, major employers, and planned infrastructure projects. Market context directly influences the reliability of income and expense projections.

Evaluating Broader Economic Factors

Monitor national and regional indicators such as employment statistics, population migration patterns, and prevailing interest rates. These elements help forecast how external forces may affect property performance over the holding period.

Obtaining Property-Specific Details

Request surveys, title reports, zoning documentation, and historical maintenance records. Schedule physical inspections to identify deferred maintenance or structural concerns. Comprehensive property knowledge prevents surprises later in the process.

Analyzing Income Streams and Operating Expenses

Estimating Potential Gross Income

Start with actual collected rent, then adjust for market-supported rents and anticipated lease escalations. Include revenue from parking, laundry, storage, or other ancillary sources. Conservative estimates protect against overly optimistic projections.

Determining Effective Gross Income

Subtract a realistic vacancy and credit loss allowance from potential gross income. Industry standards or local data guide the appropriate percentage. This adjustment reflects real-world collection challenges.

Itemizing and Validating Operating Expenses

List property taxes, insurance, utilities, management fees, maintenance, and administrative costs. Cross-check against historical statements and industry benchmarks. Reserves for replacements should be included to cover future capital needs.

Calculating Net Operating Income (NOI)

Subtract stabilized operating expenses from effective gross income to determine NOI. NOI serves as the cornerstone metric for most valuation methods. Consistent NOI calculation is central to learning how to underwrite a real estate deal.

Assessing Debt Service and Cash Flow

Modeling Financing Scenarios

Input current loan terms, including interest rate, amortization period, and loan-to-value ratio. Calculate annual debt service and the resulting debt-service-coverage ratio. Multiple scenarios help evaluate sensitivity to rate changes.

Projecting Annual Cash Flow Before Tax

Subtract debt service from NOI to arrive at cash flow before tax. Positive and growing cash flow indicates a healthier investment. Track this metric year by year throughout the projected hold period.

Calculating Key Return Metrics

Compute cash-on-cash return, internal rate of return (IRR), and equity multiple. These figures allow comparison across different investment opportunities. Return metrics provide objective evidence when deciding how to underwrite a real estate deal.

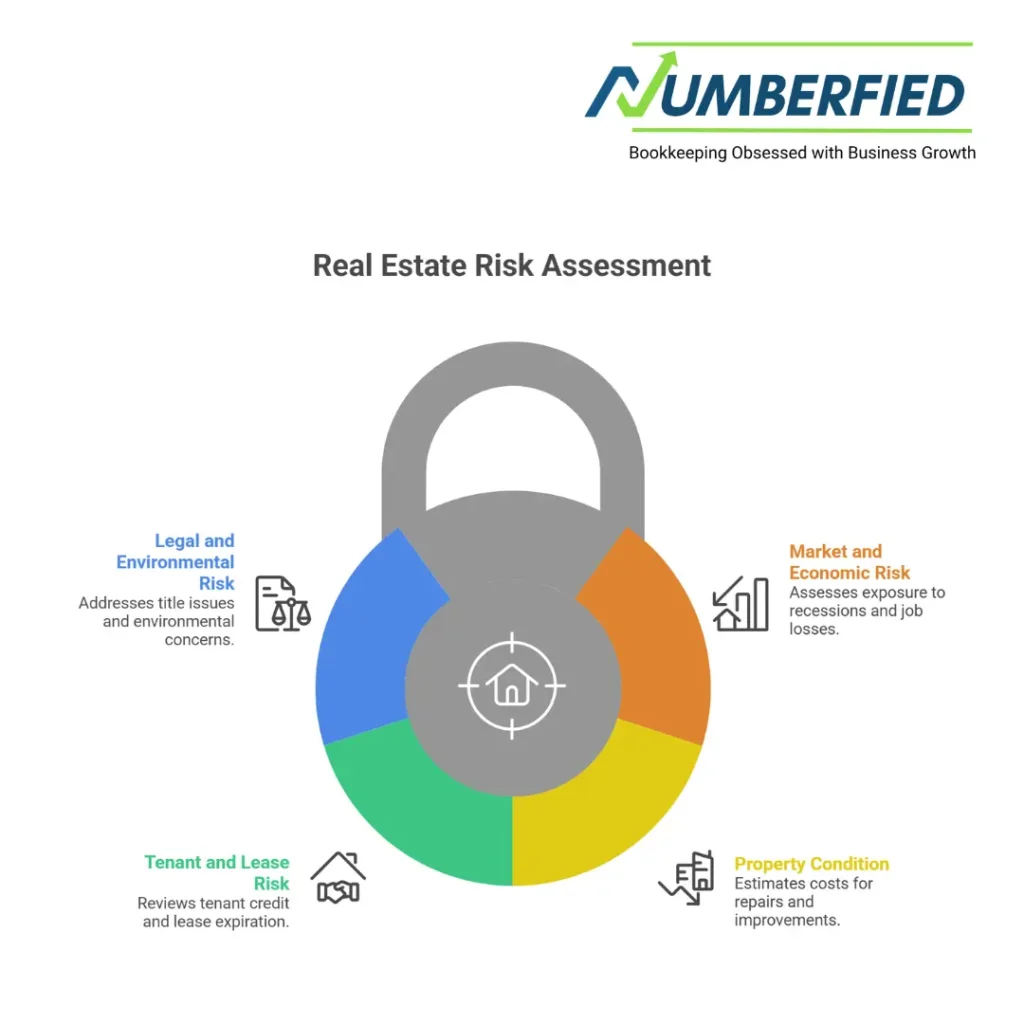

Identifying and Quantifying Risks

Market and Economic Risk Factors

Assess exposure to recessions, job losses in the area, or oversupply of competing properties. Consider how long it might take to re-lease space if tenants vacate. Market risk evaluation strengthens overall underwriting conclusions.

Property Condition and Capital Needs

Estimate costs for immediate repairs and planned capital improvements over the next five to ten years. Underestimating capital expenditures is a frequent cause of reduced returns. Detailed reserve planning is a best practice.

Tenant and Lease-Related Risks

Review tenant credit quality, lease expiration schedules, and renewal probabilities. For commercial properties, analyze the business stability of major tenants. Tenant risk directly impacts income stability.

Legal, Title, and Environmental Concerns

Order title commitments and review for encumbrances or unresolved disputes. Perform environmental due diligence appropriate to the property type and history. Addressing these issues early avoids costly post-closing problems.

Building and Using Underwriting Models

Starting with Spreadsheet-Based Analysis

Use Excel or Google Sheets to create templates that automatically calculate NOI, cash flow, and return metrics. Include sections for income, expenses, debt, and exit assumptions. Spreadsheets remain accessible and customizable for most investors.

Exploring Specialized Underwriting Software

Consider professional tools such as Argus, RealData, or PropertyMetrics for more complex deals. These platforms handle partnership structures, waterfalls, and detailed cash-flow modeling. Software can increase efficiency as deal volume grows.

Applying Standard Valuation Approaches

Calculate capitalization rate, gross rent multiplier, and discounted cash flow value. Compare the indicated values against the asking price to gauge reasonableness. Multiple approaches provide a range of value estimates.

Validating Model Assumptions and Outputs

Perform sensitivity and scenario analysis by adjusting vacancy, expense growth, and exit cap rates. Compare results against industry benchmarks. Validation confirms the reliability of your underwriting conclusions.

Reaching an Investment Decision

Interpreting Underwriting Results Holistically

Review whether projected returns meet or exceed your investment criteria and risk tolerance. Consider qualitative factors alongside quantitative outputs. Holistic interpretation leads to well-reasoned decisions.

Ranking and Comparing Investment Opportunities

Standardize underwriting outputs to facilitate side-by-side comparison of multiple properties. Prioritize deals that offer the strongest risk-adjusted returns. Objective ranking removes emotion from the selection process.

Negotiating Terms Using Underwriting Insights

Present data-driven arguments for price adjustments, seller credits, or improved financing terms. Underwriting findings carry significant weight in negotiations. Effective use of analysis often improves deal economics.

Planning for Ongoing Performance Monitoring

Establish procedures to compare actual results against underwriting projections quarterly or annually. Update models when significant variances occur. Continuous monitoring allows for timely corrective action.

Conclusion

Mastering how to underwrite a real estate deal equips you with the knowledge and discipline required to build and maintain a successful investment portfolio in any market condition. By systematically gathering data, analyzing financials, evaluating risks, and applying sound valuation methods, you position yourself to make decisions with clarity and confidence.

We invite you to put these principles into practice on your next opportunity, and if you would like expert assistance tailoring the process to your specific goals, reach out to the team at Numberfied.

FAQs

What is the first step when learning how to underwrite a real estate deal?

Collect and verify all financial documents, including rent rolls and operating statements. Organize data clearly for accurate analysis. Start with historical performance before making forward-looking projections.

How much vacancy should I assume during underwriting?

Use local market data or historical property performance to determine a realistic vacancy rate. Many investors apply 5–10% depending on asset class and location. Avoid using zero vacancy unless fully leased long-term.

Why is NOI considered the most important metric in underwriting?

NOI represents the property’s ability to generate income after operating expenses but before debt. Lenders and investors rely on NOI for valuation and coverage ratio calculations. Accurate NOI drives most return projections.

How do I account for future capital expenditures in my model?

Create a replacement reserve schedule based on property age, condition, and industry guidelines. Allocate annual amounts for major items like roofs or HVAC systems. This ensures realistic cash flow projections over the hold period.

What tools are best for beginners learning how to underwrite a real estate deal?

Start with simple Excel templates that handle basic calculations for income, expenses, and returns. Free online resources offer customizable models. Practice with sample deals to build confidence before using advanced software.

How do interest rate changes impact underwriting?

Rising rates increase debt service costs, reducing cash flow and returns. Model scenarios with higher rates to test viability. Fixed-rate loans can provide stability in volatile environments.

What is sensitivity analysis, and why is it useful?

It tests how changes in key assumptions affect returns and cash flow. Adjusting vacancy or expenses reveals the deal’s resilience. This helps identify risks and set conservative expectations.

How does underwriting differ for multifamily versus single-family properties?

Multifamily focuses on unit mix, economies of scale, and tenant turnover. Single-family homes emphasize location appeal and resale value. Adjust models to reflect these differences in income stability.

When should I walk away from a deal during underwriting?

If projected returns fall below your minimum thresholds or risks outweigh rewards. Red flags include poor market trends or significant undisclosed issues. Trust the numbers and your analysis.

How often should I update my underwriting model after closing?

Review performance quarterly and update annually or when major changes occur. Compare actuals to projections to refine future assumptions. Ongoing monitoring improves accuracy over time.

Read Also: 9 Surprising Ways a Bookkeeping Service for Small Business Can Boost Your Success