Introduction

In the dynamic world of property investments, real estate underwriting stands as a critical process that ensures sound financial decisions. This evaluation method helps lenders and investors assess the viability of real estate deals, minimizing risks while maximizing potential returns. Whether you are a seasoned investor or a first-time lender, understanding real estate underwriting can empower you to navigate the complexities of the market with confidence. At Numberfied, we believe in providing clear insights to help you achieve your goals. In this guide, we explore the fundamentals, offering practical advice to enhance your approach.

- Real estate underwriting involves a thorough analysis of property value, borrower capability, and market conditions to determine loan feasibility.

- It plays a vital role in preventing financial losses by identifying potential risks early in the transaction.

- Effective underwriting leads to better investment outcomes, fostering long-term stability in your portfolio.

- By mastering this process, you can align your strategies with current economic trends across the US.

- Professional tools and expertise can streamline underwriting, saving time and resources for all stakeholders.

Understanding the Basics of Real Estate Underwriting

Definition and Core Principles

Real estate underwriting refers to the systematic review of factors influencing a property’s financial performance. It begins with establishing clear criteria for approval, ensuring that every aspect aligns with regulatory standards. This foundation helps in creating a balanced assessment that supports sustainable lending practices.

Historical Evolution in the US Market

Over the decades, real estate underwriting has evolved from simple appraisals to sophisticated models incorporating economic data. In the US, post-2008 financial reforms have emphasized transparency and risk management. Today, it integrates technology to provide more accurate predictions for property investments.

Common Misconceptions Clarified

Many believe underwriting is solely about credit scores, but it encompasses broader elements like location and income potential. Another myth is that it’s a quick process; in reality, it requires detailed documentation and analysis. Addressing these helps readers approach it with realistic expectations.

Role in Modern Financing

In contemporary deals, underwriting serves as a bridge between borrowers and lenders, facilitating secure transactions. It adapts to diverse property types, from residential to commercial. This adaptability ensures relevance in varying economic climates across states.

Key Components Involved in Real Estate Underwriting

Property Valuation Techniques

Accurate valuation is central to underwriting, using methods like comparable sales analysis. Appraisers consider recent transactions in similar areas to determine fair market value. This step prevents over-leveraging and promotes equitable lending.

Borrower Financial Assessment

Evaluating the borrower’s income, debt ratios, and credit history forms a core part of underwriting. Lenders review tax returns and employment stability to gauge repayment ability. This comprehensive check builds trust in the financial partnership.

Market and Economic Analysis

Real estate underwriting includes studying local market trends, such as supply and demand dynamics. Economic indicators like employment rates influence projections. Understanding these factors helps predict long-term property performance in different US regions.

Legal and Regulatory Compliance

Ensuring adherence to laws, including zoning regulations and environmental standards, is essential in underwriting. Documentation verifies title clarity and insurance coverage. This protects all parties from future legal disputes.

The Step-by-Step Process of Real Estate Underwriting

Initial Application Review

The process starts with gathering borrower information and property details for preliminary screening. Real estate underwriting at this stage identifies any immediate red flags. An efficient review sets the tone for a smooth progression.

Data Collection and Verification

Compiling documents like financial statements and property surveys is crucial in underwriting. Verification involves cross-checking with third-party sources for accuracy. This diligence reduces errors and enhances decision-making.

Risk Assessment and Modeling

Using quantitative models, underwriters simulate various scenarios to evaluate risks. Real estate underwriting incorporates stress testing for economic downturns. These insights guide adjustments to loan terms for better security.

Final Decision and Approval

After analysis, the underwriter recommends approval, denial, or modifications. Underwriting culminates in a detailed report justifying the outcome. This transparency aids in appeals or revisions if needed.

Tools and Technologies Enhancing Real Estate Underwriting

Software Solutions for Efficiency

Modern platforms automate data entry and analysis in real estate underwriting, reducing manual errors. Features like AI-driven predictions offer faster insights. These tools are accessible to professionals nationwide, improving workflow.

Data Analytics and Big Data Integration

Incorporating vast datasets from public records enhances underwriting precision. Analytics reveal patterns in market behavior. This approach supports proactive strategies in volatile environments.

AI and Machine Learning Applications

AI algorithms process complex variables quickly during underwriting. They identify anomalies in financial data. Adopting these technologies leads to more informed and timely decisions.

Integration with CRM Systems

Linking underwriting tools with customer relationship management streamlines communication. Real estate underwriting benefits from real-time updates on client status. This fosters better collaboration among teams.

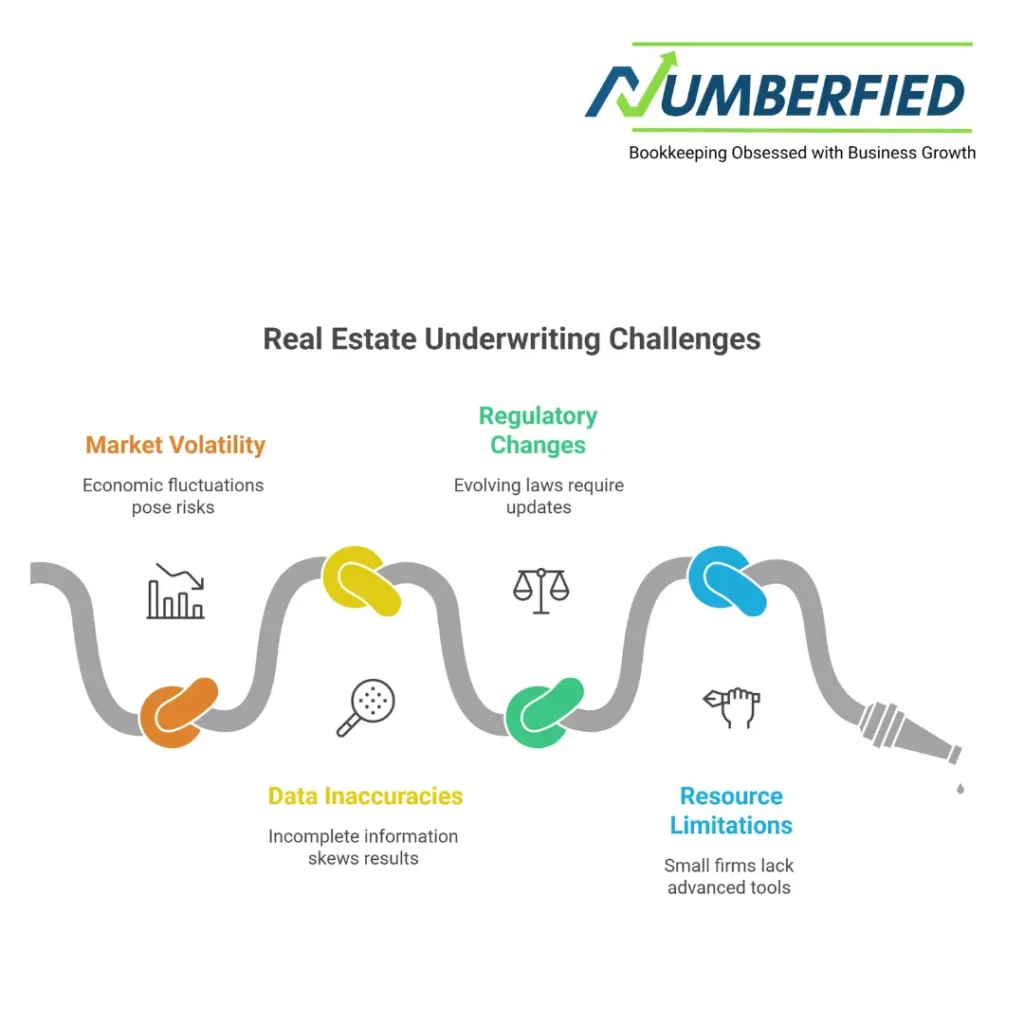

Challenges and Solutions in Real Estate Underwriting

Navigating Market Volatility

Economic fluctuations pose risks, but underwriting counters this with diversified data sources. Monitoring national indicators helps anticipate changes. Adaptive strategies maintain stability in investments.

Addressing Data Inaccuracies

Incomplete information can skew results, so underwriting emphasizes robust verification protocols. Training programs for staff improve accuracy. Regular audits ensure ongoing reliability.

Managing Regulatory Changes

Evolving laws require constant updates in underwriting practices. Staying informed through industry associations is key. Compliance software automates tracking of new requirements.

Overcoming Resource Limitations

Small firms may lack advanced tools, but outsourcing elements of real estate underwriting can help. Partnerships with tech providers offer cost-effective solutions. This levels the playing field for all US entities.

Best Practices for Effective Real Estate Underwriting

Emphasizing Thorough Documentation

Maintaining detailed records is a cornerstone of successful real estate underwriting. It facilitates quick reviews and audits. Organized files support faster closings and reduce disputes.

Fostering Team Collaboration

Involving multidisciplinary experts enhances real estate underwriting outcomes. Regular meetings align perspectives on risks. This collective approach yields comprehensive evaluations.

Continuous Education and Training

Keeping skills current through workshops benefits real estate underwriting professionals. Certifications in finance and real estate deepen expertise. Lifelong learning adapts to industry advancements.

Implementing Quality Control Measures

Routine checks and peer reviews strengthen real estate underwriting processes. Feedback loops identify improvement areas. These practices elevate overall performance standards.

Advanced Strategies in Real Estate Underwriting

Portfolio Diversification Techniques

Spreading investments across property types mitigates risks in real estate underwriting. Analysis of regional variations informs selections. This strategy promotes balanced growth.

Scenario Planning and Forecasting

Developing multiple future models is advanced in real estate underwriting. It prepares for uncertainties like interest rate shifts. Accurate forecasting aids strategic planning.

Sustainability and ESG Considerations

Incorporating environmental factors is emerging in real estate underwriting. Assessing green building standards adds value. This aligns with growing investor preferences for responsible practices.

Leveraging International Benchmarks

While focused on the US, comparing with global trends enriches real estate underwriting. Insights from stable markets inform local adaptations. This broadens analytical perspectives.

Conclusion

Real estate underwriting remains an indispensable element in securing prosperous property ventures, offering a structured path to evaluate and mitigate risks. By grasping its components, processes, and best practices, you can make more informed choices that align with your financial objectives. Remember, effective real estate underwriting not only protects investments but also unlocks opportunities in the ever-evolving US real estate landscape. We at Numberfied are here to assist with expert guidance tailored to your needs. Contact us today to explore how we can support your next project.

Frequently Asked Questions

What is the primary goal of real estate underwriting?

The main objective is to assess the financial viability of a property loan or investment by examining risks and returns. This ensures lenders provide funding only to sustainable deals, protecting capital. Readers benefit from understanding this to approach financing with confidence.

How long does real estate underwriting typically take?

The duration varies from two weeks to a month, depending on deal complexity and documentation completeness. Factors like market conditions can influence timelines. Preparing thorough applications in advance can expedite the process for borrowers.

What documents are required for real estate underwriting?

Essential items include financial statements, tax returns, property appraisals, and title reports. These verify borrower credibility and asset value. Gathering them early streamlines approval and reduces delays.

Can real estate underwriting be automated?

Partial automation through software handles data analysis and risk modeling efficiently. However, human oversight remains crucial for nuanced judgments. This blend enhances accuracy while saving time for professionals.

What role does a credit score play in real estate underwriting?

It indicates borrower reliability in repaying debts, influencing loan terms. Higher scores often lead to better rates and approvals. Improving your credit beforehand can strengthen your position in applications.

How does location impact real estate underwriting?

Geographic factors affect property value and market stability, with urban areas often showing higher potential. Underwriters analyze local economics and trends. This helps investors choose promising sites across the US.

What are the common risks identified in real estate underwriting?

Key concerns include market downturns, borrower default, and environmental issues. Early detection allows for mitigation strategies. Awareness of these enables better-prepared investment decisions.

Is real estate underwriting different for commercial properties?

Yes, it involves more complex analyses like tenant leases and cash flow projections. Residential focuses on individual borrowers. Understanding distinctions aids in tailoring approaches to property types.

How can technology improve real estate underwriting?

Tools like AI provide faster data processing and predictive insights. They reduce errors and enhance decision-making. Adopting them leads to more efficient operations for lenders and investors.

What happens if real estate underwriting reveals issues?

Underwriters may require adjustments, such as lower loan amounts or additional collateral. In severe cases, denial occurs. Addressing findings promptly can often resolve concerns and proceed with the deal.

Read Also: 7 Insider Tips to Simplify Your Finances with QuickBooks Bookkeeping Services for Small Businesses