Introduction

Underwriting real estate stands as one of the most critical skills any investor can develop. When you underwrite real estate, you systematically analyze a property’s financial performance, market position, physical condition, and risk profile to determine whether it represents a sound investment opportunity. This disciplined process helps separate promising deals from those that could lead to financial strain or loss. In an ever-changing real estate landscape filled with fluctuating interest rates, shifting tenant demands, and evolving regulations, the ability to underwrite real estate accurately has become essential for long-term success.

We believe that clear, actionable knowledge empowers investors to make better choices and build stronger portfolios. This guide walks you through the entire underwriting process from foundational concepts to advanced techniques while providing practical insights you can apply immediately. By the end, you will understand exactly how to underwrite real estate with greater confidence and precision.

Key Takeaways

- Underwriting real estate combines financial analysis, market research, and risk evaluation to assess investment viability.

- A structured, repeatable process helps eliminate emotion-driven decisions and improves consistency.

- Accurate data collection, realistic projections, and thorough due diligence form the backbone of reliable underwriting.

- Common errors, such as ignoring vacancy trends or underestimating capex, can be avoided with disciplined habits.

- Modern tools and emerging factors like sustainability increasingly influence how professionals underwrite real estate.

- Strong underwriting supports better negotiation, financing approval, and portfolio performance.

What Does It Mean to Underwrite Real Estate?

Defining the Core Concept

To underwrite real estate means to perform a detailed risk-and-return evaluation of a property before committing capital or extending credit. The goal is to verify that projected income will cover expenses, debt service (if applicable), and deliver acceptable returns while accounting for potential downsides.

The Difference Between Underwriting and Appraisal

While an appraisal focuses primarily on determining current market value, underwriting goes further by stress-testing future cash flows, occupancy assumptions, and exit strategies. Underwriting real estate, therefore, serves both buyers and lenders by answering “Is this deal sustainable over time?”

Why Underwriting Matters in Today’s Market

Rising construction costs, interest-rate volatility, and remote-work trends have made outdated assumptions dangerous. Investors who underwrite real estate rigorously are better positioned to adapt to these changes and protect their capital.

How Underwriting Fits into the Overall Investment Lifecycle

Underwriting occurs after initial deal sourcing but before final commitment. It directly influences purchase price negotiations, loan structuring, partnership agreements, and long-term hold or exit planning.

Essential Components When You Underwrite Real Estate

Income Analysis Fundamentals

Gross potential rent, vacancy allowances, collection loss estimates, and ancillary income streams must all be carefully projected. Reliable lease abstracts and rent rolls provide the starting point for accurate income underwriting.

Expense Examination and Categorization

Operating expenses, such as property management, utilities, insurance, taxes, maintenance, and reserves, require line-by-line scrutiny. Historical statements should be trended and benchmarked against market norms when you underwrite real estate.

Net Operating Income (NOI) Calculation

NOI serves as the cornerstone metric in most underwriting models. It is derived by subtracting stabilized operating expenses from effective gross income and forms the basis for capitalization rate and debt-service-coverage-ratio analysis.

Capitalization Rate Application

The cap rate converts NOI into an indication of value and helps compare properties across submarkets. Selecting an appropriate cap rate requires understanding current investor yield requirements and perceived risk.

Debt Service Coverage and Leverage Analysis

For financed deals, lenders focus heavily on the debt service coverage ratio (DSCR). Underwriting real estate includes modeling various loan terms to confirm the property can comfortably service debt under base and stress scenarios.

The Step-by-Step Process to Underwrite Real Estate

Step 1: Preliminary Screening and Data Gathering

Collect rent rolls, operating statements (trailing 12 months and prior years), lease agreements, historical capex records, tax bills, insurance certificates, and third-party reports. Organize documents early to streamline the underwriting real estate workflow.

Step 2: Market and Submarket Research

Analyze employment trends, population growth, household formation, competing inventory, absorption rates, and asking rents. This context shapes realistic rent-growth and vacancy assumptions.

Step 3: Property-Specific Physical and Legal Due Diligence

Conduct or review property condition assessments, Phase I environmental reports, title searches, survey updates, and zoning verification. Physical findings directly impact repair budgets and future capex reserves.

Step 4: Financial Modeling and Scenario Creation

Build a multi-year pro forma that projects income, expenses, debt service, and returns. Include base-case, best-case, and worst-case scenarios to test sensitivity around key variables such as rent growth, vacancy, and exit cap rates.

Step 5: Risk Identification and Mitigation Planning

Catalog major risks, economic, operational, environmental, and regulatory, and assign probability and severity ratings. Develop contingency plans or reserve buffers to address the most material threats.

Step 6: Investment Recommendation and Reporting

Synthesize findings into a clear executive summary, investment summary, sources-and-uses table, return metrics, and go/no-go recommendation. This final package communicates the rationale for proceeding (or walking away).

Tools and Software That Help You Underwrite Real Estate

Spreadsheet-Based Modeling Platforms

Advanced Excel templates remain popular because of their flexibility. Custom macros and data tables allow rapid sensitivity and scenario analysis when you underwrite real estate.

Specialized Commercial Real Estate Software

Programs such as ARGUS Enterprise, RealData, and MRI Software automate complex lease abstractions, cash-flow waterfalls, and partnership structures. These tools save time on larger or multi-tenant assets.

Market Data and Research Subscriptions

Platforms like CoStar, REIS, CBRE, and Yardi Matrix deliver rent comps, vacancy statistics, sales comparables, and economic indicators. Subscribing to credible sources ensures defensible assumptions.

Valuation and Benchmarking Resources

Accessing industry reports from NCREIF, RCA, and PwC helps place your underwriting real estate analysis within a broader market context and validates cap-rate and growth-rate selections.

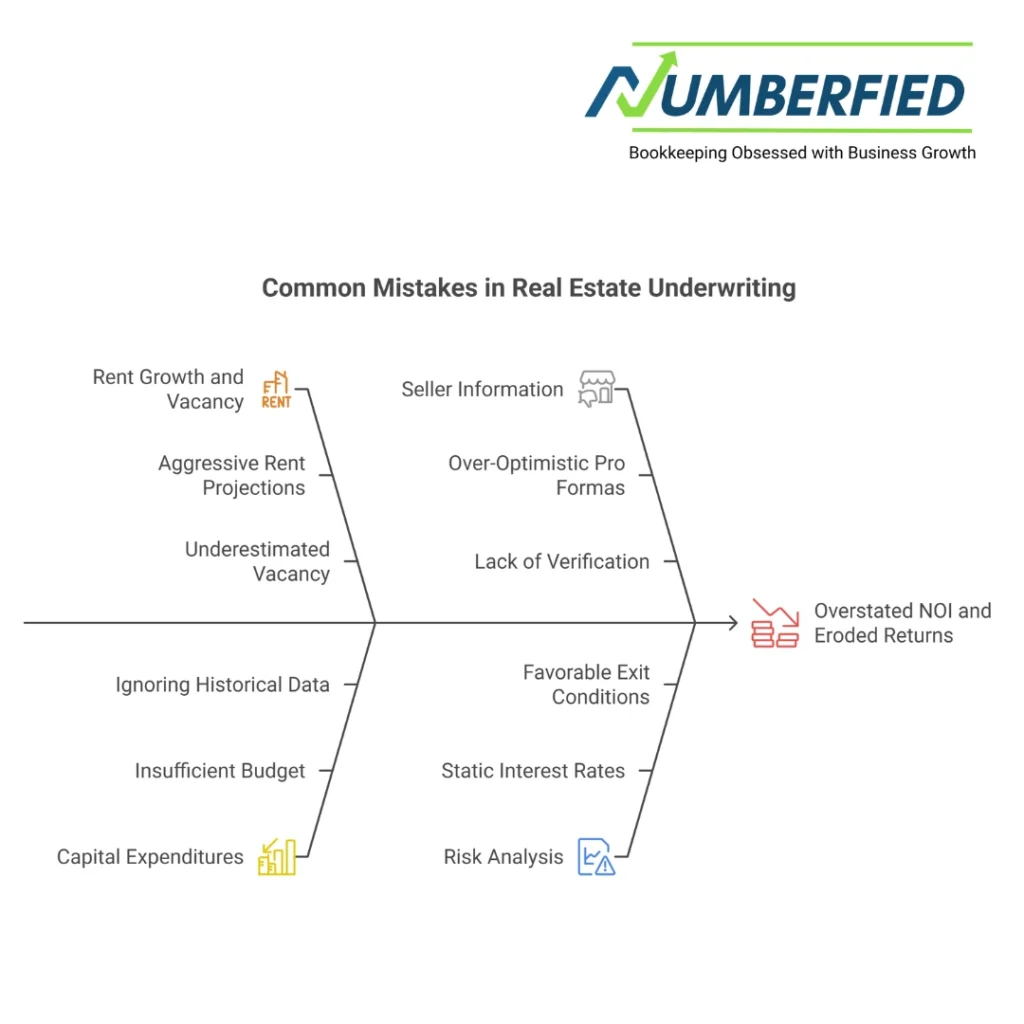

Frequent Mistakes Investors Make When Underwriting Real Estate

Assuming Unrealistic Rent Growth or Vacancy

Projecting aggressive rent increases without supporting market evidence often results in overstated NOI. Conservative, evidence-based assumptions protect against disappointment.

Underestimating Capital Expenditures

Failing to budget adequately for roof replacements, HVAC overhauls, parking resurfacing, or ADA upgrades can erode returns. Historical spending patterns and engineer reports provide realistic capex forecasts.

Over-Reliance on Seller-Provided Information

Seller pro formas often present optimistic views. Always verify numbers against audited statements, utility bills, and third-party data to underwrite real estate objectively.

Ignoring Interest-Rate and Exit Risk

Many models assume static rates and favorable exit conditions. Incorporating rate-increase scenarios and higher terminal cap rates reveals true downside protection.

Skipping Sensitivity and Break-Even Analysis

Single-point projections hide vulnerabilities. Testing ranges around critical variables clarifies how much cushion exists before returns fall below target thresholds.

Advanced Techniques to Strengthen Your Underwriting Real Estate Approach

Monte Carlo Simulation for Probabilistic Outcomes

This method runs thousands of randomized scenarios to produce probability distributions of IRR and equity multiples. It quantifies uncertainty more comprehensively than traditional sensitivity tables.

Incorporating ESG and Climate Risk Metrics

Investors and lenders increasingly require evaluation of energy efficiency, carbon footprint, flood exposure, and social impact. These factors can influence cap rates, insurability, and resale appeal.

Stress-Testing for Black-Swan Events

Modeling severe but plausible downturns, prolonged high vacancy, sharp rent declines, or major repair events helps gauge portfolio resilience when you underwrite real estate.

Portfolio Optimization and Correlation Analysis

Assessing how a new acquisition interacts with existing holdings regarding geographic concentration, tenant industry exposure, and lease rollover timing improves overall risk-adjusted returns.

Legal, Regulatory, and Compliance Factors in Underwriting Real Estate

Title and Encumbrance Review

A clean title commitment free of unexpected liens, easements, or judgments is non-negotiable. Title insurance exceptions must be resolved or appropriately underwritten.

Zoning, Entitlements, and Land-Use Compliance

Confirming current and allowable uses prevents surprises related to nonconforming status or future development restrictions.

Fair Housing, ADA, and Local Ordinance Adherence

Ensuring the property complies with accessibility requirements and nondiscrimination laws avoids future litigation risk.

Environmental Due Diligence Requirements

Phase I and, when warranted, Phase II reports identify recognized environmental conditions that could trigger costly remediation.

Tax, Insurance, and Reserve Fund Considerations

Verifying accurate tax assessments, adequate coverage limits, and sufficient operating reserves protects cash flow stability.

Conclusion

Mastering how to underwrite real estate equips you with the clarity and discipline needed to thrive in competitive and unpredictable markets. From income and expense analysis to advanced scenario modeling, regulatory compliance, and risk mitigation, each element contributes to more confident decision-making and stronger investment outcomes.

By following a structured process, leveraging reliable data and tools, and consistently avoiding common pitfalls, you position yourself to identify value, negotiate effectively, and build lasting wealth through real estate. If you would like expert support tailoring these principles to your specific deals or portfolio, reach out to the team at Numberfied. We are ready to help you underwrite real estate with greater precision and peace of mind.

FAQs

What exactly happens when you underwrite real estate?

Underwriting real estate involves detailed financial, physical, market, and legal analysis to evaluate a property’s risk and return profile. The process confirms whether projected cash flows support the asking price and financing terms. It ultimately guides a go, no-go, or renegotiate decision.

How long does it typically take to underwrite real estate?

Simple single-tenant deals may take 1–3 weeks, while complex multi-tenant or development projects can require 4–12 weeks. Time depends on data availability, third-party report turnaround, and deal complexity. Early document organization accelerates the timeline.

Is underwriting real estate only for commercial properties?

No underwriting real estate applies to residential rentals, multifamily, office, retail, industrial, and hospitality assets. The core principles remain consistent, though specific metrics and risk factors vary by property type.

What is the most important metric when you underwrite real estate?

Net Operating Income (NOI) is widely regarded as the single most important metric because it drives valuation, debt capacity, and return calculations. Accurate NOI projection requires careful income and expense validation.

How do lenders use underwriting real estate analysis?

Lenders underwrite real estate to confirm the property generates sufficient cash flow to cover debt service, usually targeting a minimum DSCR of 1.20–1.35x. They also assess loan-to-value ratios and sponsor experience before approving financing.

Can you underwrite real estate without hiring professionals?

Yes, many experienced investors underwrite real estate independently using spreadsheets, public data, and market reports. However, engaging appraisers, engineers, and attorneys for larger or unfamiliar deals reduces blind spots and risk.

Why include capex reserves when you underwrite real estate?

Capital expenditure reserves account for future replacements and major repairs that are not annual operating expenses. Omitting them inflates short-term cash flow and misrepresents true economic returns over the hold period.

How do interest-rate changes affect underwriting real estate?

Higher interest rates increase debt service costs, lower DSCR, and can compress purchase prices as cap rates expand. Stress-testing models with rising-rate scenarios reveals how sensitive returns are to borrowing costs.

What role does location play when you underwrite real estate?

Location heavily influences rent growth potential, vacancy risk, tenant demand, and resale liquidity. Submarket fundamentals, employment, demographics, and infrastructure must support your income and exit assumptions.

Should beginners start underwriting real estate on small deals?

Yes, smaller multifamily or single-tenant properties offer valuable learning opportunities with lower capital at risk. Practicing on modest deals builds confidence and refines modeling skills before tackling larger transactions.

Read Also: Virtual Bookkeeping Services for Small Businesses That’ll Change Your Life!