Introduction

When engaging in real estate transactions, whether as an investor seeking profitable opportunities or as a lender providing financing, the underwriting model in real estate emerges as one of the most essential analytical frameworks available to ensure that every decision rests on a solid foundation of financial and market realities. We recognize that participants in the real estate market frequently face uncertainty regarding property values, borrower reliability, cash flow sustainability, and broader economic influences, all of which the underwriting model in real estate systematically addresses by integrating quantitative metrics, qualitative assessments, and forward-looking projections into a cohesive evaluation process.

Through this comprehensive examination of the underwriting model in real estate, we aim to equip readers with a thorough understanding of its mechanics, its critical role across different property types and transaction structures, and the practical ways in which mastering this approach can lead to more confident, risk-adjusted outcomes in an industry where precision and foresight directly translate into long-term success.

Key Takeaways

- The underwriting model in real estate serves as a disciplined methodology that combines detailed financial analysis, property-specific evaluation, and macroeconomic context to determine the overall soundness of any proposed real estate investment or loan.

- Effective application of the underwriting model in real estate enables stakeholders to identify potential vulnerabilities early, structure transactions more securely, and allocate capital toward opportunities that demonstrate the strongest probability of performing as expected.

- Continuous refinement of underwriting practices, including the incorporation of advanced data sources and analytical techniques, remains essential for maintaining relevance and accuracy in rapidly evolving market environments.

What Is the Underwriting Model in Real Estate?

The underwriting model in real estate constitutes a structured, repeatable analytical framework designed specifically to assess whether a particular property financing arrangement or investment proposal meets the necessary criteria for safety, profitability, and alignment with institutional or individual objectives. Rather than representing a single formula, this model encompasses a comprehensive set of procedures, metrics, and judgment criteria that collectively produce an informed recommendation regarding approval, modification, or rejection of the transaction under consideration.

Core Definition and Strategic Objectives

At its foundation, the underwriting model in real estate systematically evaluates the interplay between expected income streams, operating expenses, debt obligations, collateral quality, borrower capacity, and external market forces in order to forecast the likelihood of sustained performance throughout the life of the investment or loan. The primary strategic objectives include protecting principal, achieving appropriate risk-adjusted returns, ensuring regulatory compliance, and maintaining portfolio stability across varying economic cycles.

Primary Stakeholders and Their Distinct Perspectives

A wide array of participants, including commercial banks, private debt funds, Fannie Mae and Freddie Mac conduits, life insurance companies, real estate investment trusts, and individual high-net-worth investors, rely upon versions of the underwriting model in real estate that have been customized to reflect their unique risk tolerances, return thresholds, regulatory constraints, and investment horizons. While institutional lenders typically emphasize conservative leverage ratios and strong debt service coverage, opportunistic investors may apply more flexible interpretations of the same model when pursuing value-add or development strategies.

Fundamental Principles That Ensure Reliability

Consistency across similar transactions, independence of analysis from origination pressures, thorough documentation of every material assumption, and reliance on verifiable third-party data represent the foundational principles that underpin every credible application of the underwriting model in real estate, thereby fostering trust in the resulting credit decisions and investment conclusions.

Major Types of Underwriting Models in Real Estate

Over time, several distinct approaches to the underwriting model in real estate have developed in response to differences in property complexity, transaction volume, regulatory environment, and technological capability, each offering particular advantages depending on the context in which it is deployed.

Manual and Traditional Underwriting Methodologies

Manual underwriting continues to serve as the preferred approach whenever transactions involve unique characteristics, transitional properties, complex ownership structures, or specialized asset classes that require nuanced professional judgment beyond what standardized algorithms can adequately capture. Experienced underwriters meticulously review historical performance records, interview key principals, conduct detailed site inspections, and apply seasoned insight to arrive at well-supported conclusions.

Automated Underwriting Systems and Their Widespread Adoption

Automated underwriting systems, which rely upon sophisticated rule engines, statistical scoring models, and large historical datasets, have become the dominant method for processing high volumes of conforming residential mortgages and certain lower-risk small-balance commercial loans because they deliver rapid, consistent preliminary decisions while significantly reducing processing costs and turnaround times. These systems excel particularly when dealing with standardized documentation and predictable risk profiles.

Hybrid Models That Balance Efficiency and Expertise

Recognizing the limitations inherent in purely automated or purely manual processes, many leading institutions now implement hybrid underwriting models in real estate that automatically handle routine verifications, initial risk scoring, and document classification while reserving final credit judgment and exception approvals for senior underwriters who possess deep market knowledge and transaction experience.

Step-by-Step Underwriting Process in Real Estate

A clearly defined, sequential workflow ensures that every application of the underwriting model in real estate proceeds in an orderly, comprehensive manner that minimizes the possibility of material oversights.

Initial Application Intake and Eligibility Screening

The process commences with a thorough review of the submitted loan application package to confirm that minimum threshold criteria, such as minimum credit score, maximum loan-to-value ratio, required debt-service coverage, property eligibility, and geographic acceptability, are satisfied before committing significant resources to deeper analysis.

Comprehensive Collection and Verification of Supporting Documentation

Once preliminary eligibility has been established, underwriters systematically gather and independently verify an extensive array of financial statements, rent rolls, leases, title commitments, zoning reports, environmental assessments, engineering studies, and third-party appraisals that collectively form the evidentiary foundation for all subsequent analytical steps.

In-Depth Financial Modeling and Collateral Evaluation

During this critical phase, detailed pro forma cash flow projections are constructed under multiple scenarios, key performance metrics such as debt service coverage ratio, loan constant, break-even occupancy, and yield on cost are calculated, and independent appraisals are reconciled against purchase prices or stated values to confirm adequate collateral protection.

Final Risk Rating, Structuring Recommendations, and Credit Decision

The underwriting model in real estate concludes with an overall risk rating assignment, identification of any necessary covenants or structural adjustments, preparation of a comprehensive credit memorandum, and issuance of a final credit decision that may range from full approval to structured conditional commitment or outright denial accompanied by a detailed rationale.

Critical Factors Evaluated in Real Estate Underwriting Models

Underwriters must weigh an extensive range of interdependent quantitative and qualitative elements when applying the underwriting model in real estate to ensure that no material risk factor escapes appropriate consideration.

Borrower and Sponsor Financial Capacity and Track Record

The financial strength, liquidity position, net worth, contingent liabilities, and demonstrated real estate experience of borrowers and guarantors receive meticulous scrutiny because historical performance and current balance sheet health provide the strongest indicators of future repayment reliability.

Property-Specific Operating Performance and Physical Condition

Detailed analysis of trailing-twelve-month and projected net operating income, occupancy stability, expense trends, deferred maintenance requirements, capital expenditure reserves, and overall physical condition forms the cornerstone of the property-level evaluation within every underwriting model in real estate.

Macroeconomic and Submarket Dynamics Influencing Future Performance

Underwriters incorporate current and forecasted employment levels, population growth, household formation rates, competing supply pipelines, rental rate trends, vacancy absorption statistics, and prevailing capitalization rates to develop realistic expectations regarding the property’s ability to generate sufficient income over the loan term.

Appropriateness of Proposed Loan Structure and Protective Covenants

Careful examination of amortization periods, interest rate type and reset provisions, prepayment penalties, reserve requirements, financial reporting obligations, transfer restrictions, and other structural features ensures that the transaction remains appropriately balanced from both the borrower’s and the lender’s perspectives.

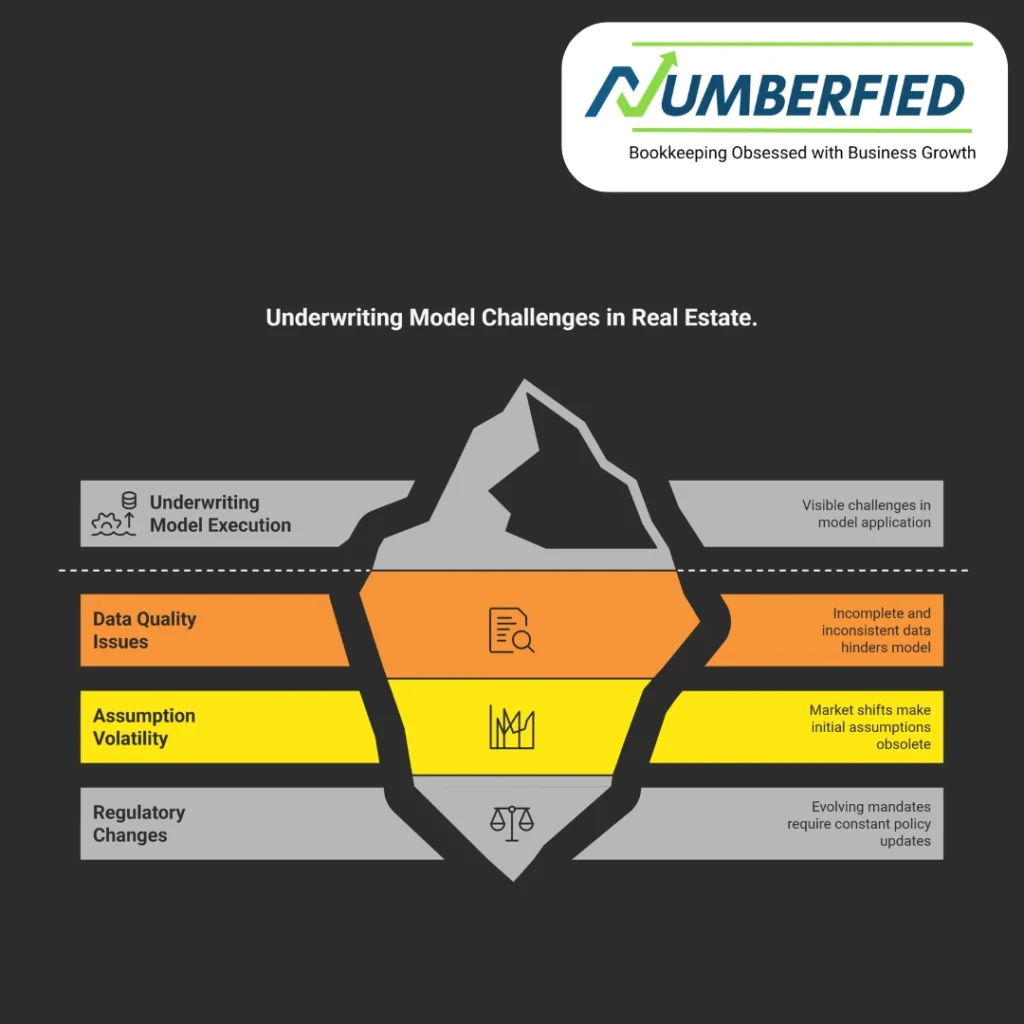

Common Challenges Encountered When Applying Underwriting Models in Real Estate

Despite best efforts to maintain rigor and objectivity, practitioners regularly confront obstacles that can complicate or delay effective execution of the underwriting model in real estate.

Persistent Issues with Data Quality and Completeness

Incomplete rent rolls, unreconciled operating statements, unverifiable sponsor financial statements, and discrepancies among various third-party reports frequently require additional time-consuming clarification rounds that extend underwriting timelines.

Difficulty Maintaining Assumptions During Periods of Market Transition

Sudden shifts in interest rates, capitalization rates, tenant demand, construction costs, or regulatory requirements can rapidly render initial underwriting assumptions obsolete, necessitating iterative re-evaluation of projected performance metrics.

Ongoing Adaptation to Evolving Regulatory and Compliance Mandates

Frequent modifications to agency guidelines, environmental disclosure rules, fair lending requirements, anti-money laundering protocols, and state-specific licensing provisions demand continuous updates to underwriting policies, procedures, and documentation standards.

Best Practices for Strengthening Underwriting Models in Real Estate

Institutions and individual practitioners that consistently achieve superior risk-adjusted performance tend to adhere to several widely recognized best practices when designing and executing the underwriting model in real estate.

Development and Rigorous Enforcement of Standardized Templates and Checklists

Comprehensive, regularly updated underwriting templates, review checklists, and exception tracking logs promote consistency, reduce the likelihood of material omissions, and facilitate efficient quality control across large teams.

Incorporation of Rigorous Scenario and Sensitivity Testing

Systematic evaluation of base-case, downside, and stress-case projections, including interest rate increases, occupancy declines, expense inflation, and lease rollover assumptions, provides critical insight into transaction resiliency under adverse conditions.

Commitment to Independent Third-Party Verification and Expert Consultation

Engaging qualified, independent appraisers, environmental consultants, structural engineers, property condition assessors, and market research firms ensures that key inputs remain objective and defensible.

Investment in Continuous Professional Development for Underwriting Teams

Regular training on emerging market trends, new analytical methodologies, updated regulatory requirements, and advanced software tools maintains the technical proficiency and market awareness necessary for high-quality underwriting execution.

Emerging Trends Reshaping Underwriting Models in Real Estate

Rapid technological advancement and changing risk landscapes continue to drive meaningful evolution in how the underwriting model in real estate is constructed, implemented, and monitored over time.

Growing Utilization of Machine Learning and Predictive Analytics

Sophisticated algorithms trained on vast historical performance databases now assist underwriters in identifying subtle patterns, improving loss prediction accuracy, and automating portions of the risk scoring process.

Expansion of Alternative and Non-Traditional Data Sources

Incorporation of utility payment histories, residential rent reporting services, satellite imagery for property condition monitoring, foot-traffic analytics, and social sentiment indicators enriches the informational foundation available to underwriters.

Increasing Weight Assigned to Environmental, Social, and Governance Considerations

Climate risk assessments, energy performance certifications, flood zone exposure analyses, and social impact evaluations increasingly influence loan pricing, covenant structures, and overall transaction approvability.

Transition Toward Real-Time Performance Monitoring Post-Closing

Advanced portfolio surveillance platforms that continuously track key operating metrics, trigger early-warning alerts, and facilitate proactive intervention represent the next frontier in extending the underwriting model in real estate beyond origination.

Conclusion

The underwriting model in real estate remains an indispensable discipline that enables lenders, investors, and other market participants to navigate the inherent uncertainties of property financing with greater clarity, discipline, and confidence. By thoroughly understanding its core components, mastering its analytical techniques, confronting its persistent challenges, adopting proven best practices, and staying attuned to emerging innovations, stakeholders position themselves to make consistently superior capital allocation decisions that enhance portfolio performance while appropriately controlling downside exposure.

Should you wish to discuss how these principles can be applied to your specific real estate opportunities or explore ways to refine your current underwriting approach for improved outcomes, we warmly invite you to connect with us at numberfied, where our experienced professionals stand ready to provide tailored guidance and practical support.

FAQs

What is the main goal of the underwriting model in real estate?

The main goal is to determine whether a real estate loan or investment is financially viable and acceptable in terms of risk. Underwriters carefully review projected cash flows, the property’s value as collateral, the borrower’s financial strength and credit history, and current market and economic conditions to decide if the deal can safely repay the debt.

Who uses the underwriting model in real estate most often?

Commercial banks, private lenders, and hard-money lenders use it on almost every deal. Fannie Mae, Freddie Mac, life insurance companies, CMBS conduits, REITs, and sophisticated individual or institutional investors also rely on underwriting to evaluate, price, and approve real estate transactions.

What is the difference between manual and automated underwriting?

Manual underwriting depends on experienced underwriters who apply professional judgment and flexibility, especially for complex or non-standard commercial deals. Automated underwriting uses rule-based software and statistical models to quickly process and approve standardized residential mortgages with consistent, predictable data.

How long does underwriting usually take?

Residential mortgage underwriting typically takes 30–45 days from application to clear-to-close, assuming standard documentation is provided. Commercial real estate underwriting often takes 60–90 days or longer due to detailed financial modeling, third-party reports (appraisals, environmental studies), sponsor background checks, and lender committee approvals.

Why is the debt service coverage ratio important?

The DSCR (net operating income ÷ annual debt service) shows whether the property generates enough cash flow to cover loan payments comfortably. Lenders generally require a minimum of 1.20x–1.35x (sometimes higher for riskier properties) to provide a cushion against vacancies, rising expenses, or drops in revenue.

Why are independent appraisals required?

An independent, third-party appraisal delivers an objective, market-supported estimate of the property’s value, protecting the lender from over-lending. It confirms sufficient collateral coverage and is required by federal regulations (such as FIRREA) and most lender policies.

How do rising interest rates affect underwriting?

Higher interest rates increase monthly and annual debt-service payments, which lowers the DSCR and reduces the maximum loan amount the property’s income can support. Underwriters may also apply more conservative cap rates, resulting in lower appraised values and tighter loan sizing overall.

What happens if underwriting standards are not met?

The lender may reduce the loan-to-value ratio or loan amount, require more borrower cash/equity, demand additional reserves, shorten the amortization period, raise the interest rate, or add stricter covenants. If critical metrics (DSCR, LTV, sponsor experience) still fall short, the loan is often declined outright.

Does sponsor experience matter in underwriting?

Yes a sponsor with a strong, proven track record managing similar property types in the same markets and through different economic cycles inspires much greater lender confidence. Experienced sponsors frequently receive higher leverage, lower reserve requirements, more flexible terms, and better overall pricing.

Why is environmental due diligence included?

Environmental assessments (Phase I and, if needed, Phase II) identify potential contamination, hazardous substances, or regulatory compliance problems that could significantly lower property value, create large cleanup costs, or expose the owner/lender to long-term liability. Unresolved environmental issues discovered late can derail a deal or force major changes to loan terms.

Read Also: Why Numberfied’s Accounting Bookkeeping Service Saves Small Businesses Time and Money