Introduction

Underwriting real estate plays a crucial role in ensuring that property investments are sound and sustainable. As professionals in the financial sector, we recognize how this process helps mitigate risks and supports confident decision-making for buyers, investors, and lenders across the United States. Whether you are purchasing your first home or expanding a commercial portfolio, grasping the fundamentals of underwriting real estate can empower you to navigate the market effectively. In this guide, we provide detailed insights into the procedures, considerations, and strategies involved, offering practical advice to address common concerns and achieve favorable outcomes.

Key Takeaways:

- Underwriting real estate involves a thorough evaluation of financial, legal, and market aspects to assess viability.

- Key factors include creditworthiness, property valuation, and economic conditions.

- Effective underwriting reduces risks and enhances investment returns.

- Technology is transforming the process for greater efficiency and accuracy.

- Staying informed on trends helps adapt to changing real estate dynamics.

- Professional guidance can streamline underwriting for better results.

What Is Underwriting Real Estate?

Underwriting real estate refers to the systematic assessment conducted by lenders or investors to determine the feasibility of financing a property transaction. This evaluation ensures that the deal aligns with financial standards and minimizes potential losses. We emphasize that understanding this concept is essential for anyone involved in real estate, as it forms the foundation of secure transactions.

The Purpose of Underwriting in Property Deals

The primary goal of real estate underwriting is to verify that the borrower can repay the loan and that the property’s value supports the investment. This step protects all parties by identifying risks early. For instance, it helps lenders approve loans that are likely to perform well over time.

Differences Between Residential and Commercial Underwriting

In residential real estate underwriting, the focus often centers on individual credit scores and income stability. Commercial underwriting, however, evaluates business cash flows and tenant leases more intensively. Recognizing these distinctions allows investors to prepare appropriately for each type.

Key Participants in the Underwriting Process

Lenders, appraisers, and title companies are central to underwriting real estate. Their collaboration ensures comprehensive reviews. Borrowers also play a role by providing accurate documentation to facilitate smooth evaluations.

The Underwriting Real Estate Process Step by Step

Navigating underwriting in real estate requires a structured approach, from initial application reviews to final approvals. We guide you through each phase to demystify the procedure and highlight where preparation can make a difference.

Initial Application and Documentation Review

The process starts with submitting financial statements, tax returns, and property details for underwriting real estate. Lenders scrutinize these to gauge preliminary eligibility. Thorough preparation here can expedite subsequent steps.

Property Appraisal and Valuation

A professional appraisal determines the property’s market value during real estate underwriting, ensuring the loan amount does not exceed the property’s value. This step involves comparable sales analysis and condition assessments. Accurate valuations prevent over-leveraging.

Credit and Financial Analysis

Underwriting real estate includes a deep dive into credit history, debt-to-income ratios, and liquidity. This analysis predicts repayment capability. Maintaining strong financial health is key to positive outcomes.

Risk Assessment and Mitigation Strategies

Identifying potential risks, such as market volatility or environmental issues, is integral to underwriting real estate. Strategies like insurance or reserves are recommended to address them. Proactive mitigation enhances deal security.

Final Decision and Loan Closing

The culmination of underwriting real estate is the approval or denial, followed by closing if approved. This phase involves legal reviews and fund disbursement. Understanding this endpoint helps in planning timelines.

Key Factors Considered in Underwriting Real Estate

Several critical factors influence the outcome of real estate underwriting. We explore these to provide you with actionable knowledge on what lenders prioritize, enabling better preparation.

Borrower’s Financial Profile

Income stability, assets, and liabilities are examined in underwriting real estate to assess affordability. A solid profile strengthens approval chances. Tips include reducing debts before applying.

Property Characteristics and Location

The property’s age, condition, and location are vital to underwriting real estate. Desirable locations with growth potential score higher. Researching local markets aids in selecting viable options.

Market and Economic Conditions

Underwriting real estate accounts for interest rates, employment trends, and housing supply. Favorable conditions support approvals. Monitoring economic indicators can inform timing decisions.

Legal and Regulatory Compliance

Ensuring adherence to zoning laws and title clarity is essential in underwriting real estate. Any discrepancies can halt progress. Professional legal reviews prevent compliance issues.

Environmental and Hazard Assessments

Underwriting real estate often requires checks for flood zones or contamination. These assessments protect against unforeseen costs. Obtaining necessary reports early streamlines the process.

Common Challenges in Underwriting Real Estate

Even with careful planning, obstacles can arise in real estate underwriting. We discuss frequent issues and solutions to help you overcome them effectively.

Dealing with Incomplete Documentation

Missing paperwork significantly delays real estate underwriting. Organize all required files in advance. This practice avoids unnecessary setbacks.

Addressing Low Appraisals

If the valuation falls short in underwriting real estate, renegotiate terms or appeal the appraisal. Providing additional comparables can resolve this. Patience and evidence are crucial.

Navigating Credit Issues

Poor credit can complicate real estate underwriting. Improve scores by paying bills on time and disputing errors. Long-term financial habits yield better results.

Market Volatility Impacts

Economic shifts affect underwriting real estate outcomes. Diversify investments and stay updated on trends. Flexibility in strategies mitigates these effects.

Regulatory Changes and Compliance Hurdles

Evolving laws can challenge real estate underwriting. Consult experts to ensure ongoing compliance. Regular updates keep you ahead of changes.

Best Practices for Successful Underwriting Real Estate

Adopting proven methods enhances the efficiency of real estate underwriting. We share practical advice to optimize your approach and achieve desirable results.

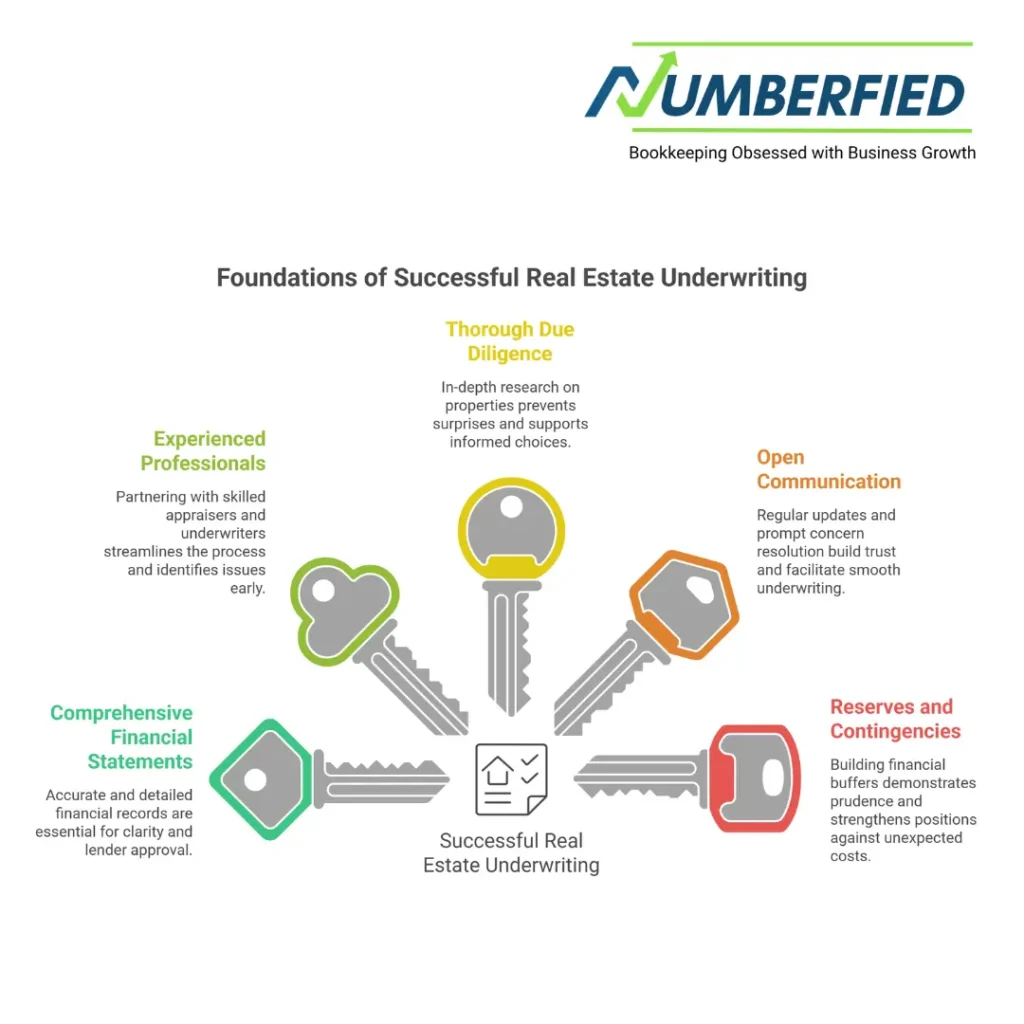

Preparing Comprehensive Financial Statements

Accurate, detailed records are foundational to underwriting real estate. Use standardized formats for clarity. This preparation impresses lenders.

Selecting Experienced Professionals

Partnering with skilled appraisers and underwriters streamlines real estate underwriting. Their expertise identifies issues early. Research credentials for reliability.

Conducting Thorough Due Diligence

In-depth research into property characteristics prevents surprises in real estate underwriting. Include site visits and historical data reviews. This diligence supports informed choices.

Maintaining Open Communication

Regular updates to all parties facilitate smooth real estate underwriting. Address concerns promptly. Transparency builds trust.

Leveraging Reserves and Contingencies

Building financial buffers strengthens positions in underwriting real estate. Plan for unexpected costs. This approach demonstrates prudence.

The Role of Technology in Underwriting Real Estate

Advancements in tools are revolutionizing real estate underwriting. We examine how innovations improve accuracy and speed, benefiting users nationwide.

Automated Valuation Models

These systems provide quick estimates for real estate underwriting, supplementing traditional appraisals. They use data analytics for precision. Adoption reduces processing times.

Data Analytics and AI Applications

AI analyzes vast datasets during real estate underwriting to predict risks. This enhances decision-making. We see increased reliability through these technologies.

Digital Documentation and E-Signatures

Streamlining paperwork digitally accelerates real estate underwriting. Secure platforms ensure compliance. Convenience is a major advantage.

Blockchain for Title and Transaction Security

Blockchain provides tamper-proof records for real estate underwriting. It minimizes fraud risks. Emerging use cases promise greater efficiency.

Integration with Real Estate Platforms

Connecting underwriting tools with listing services optimizes underwriting real estate workflows. Real-time data access improves assessments. This synergy supports faster closings.

Future Trends in Underwriting Real Estate

Looking ahead, evolving practices will shape real estate underwriting. We highlight anticipated developments to prepare you for what’s next in the US landscape.

Sustainability and Green Underwriting

Environmental criteria are gaining prominence in real estate underwriting. Energy-efficient properties receive favorable terms. Aligning with green standards boosts appeal.

Remote and Virtual Assessments

Technology enables remote evaluations in real estate underwriting. Virtual tours and drones reduce on-site needs. This trend expands accessibility.

Enhanced Risk Modeling with Big Data

Advanced analytics will refine real estate underwriting predictions. Broader data sources inform better models. Accuracy in forecasting improves.

Regulatory Evolution and Fintech Influence

New regulations and fintech innovations will transform real estate underwriting. Adaptive frameworks ensure compliance. Collaboration drives progress.

Personalized Underwriting Approaches

Tailored assessments based on individual data will personalize real estate underwriting. This customization enhances user experiences. Expect more client-centric services.

Conclusion

In summary, underwriting real estate is a vital process that safeguards investments by evaluating financial viability, property value, and market risks. By understanding its steps, key factors, and best practices, you can make more informed decisions in the dynamic US real estate market. Remember, effective underwriting of real estate not only minimizes challenges but also maximizes opportunities for success. If you seek personalized guidance to navigate this process, we invite you to contact Numberfied today for expert support.

FAQs

What does underwriting real estate entail for first-time buyers?

Underwriting real estate for first-time buyers involves reviewing credit, income, and property details to approve loans. It ensures affordability and reduces default risks. Buyers should prepare documents early to facilitate a smooth evaluation.

How long typically does the underwriting real estate process take?

The underwriting real estate process usually takes 30 to 45 days, depending on documentation completeness and market conditions. Delays can occur from appraisals or credit checks. Staying organized helps expedite approvals.

Why is property location important in underwriting real estate?

Location impacts value and risk in real estate underwriting, influencing resale potential and economic stability. Desirable areas with amenities score higher. Researching neighborhoods aids in selecting properties that meet lender criteria.

What role does the debt-to-income ratio play in underwriting real estate?

The debt-to-income ratio assesses affordability in underwriting real estate by comparing debts to earnings. Lower ratios improve approval odds. Managing debts effectively strengthens your financial profile.

How can investors handle environmental risks in underwriting real estate?

Investors address environmental risks in underwriting real estate through inspections and insurance. Identifying issues like soil contamination early prevents costs. Compliance with regulations ensures long-term viability.

What technology tools are emerging for underwriting real estate?

Emerging tools like AI and automated models enhance accuracy in real estate underwriting. They analyze data quickly for better decisions. Adopting these improves efficiency for lenders and borrowers.

How does an economic downturn affect underwriting real estate?

Economic downturns tighten underwriting standards for real estate, increasing scrutiny of finances. Lenders may require higher reserves. Monitoring trends helps time investments wisely.

What documentation is essential for commercial underwriting real estate?

Essential documents for commercial underwriting real estate include business financials, leases, and appraisals. They demonstrate cash flow stability. Accurate submissions accelerate the process.

How can borrowers appeal a denied underwriting real estate decision?

Borrowers can appeal denials in underwriting real estate by providing additional evidence or correcting errors. Consulting professionals clarifies issues. Persistence with facts often leads to reconsiderations.

What future regulations might impact the underwriting real estate?

Future regulations could emphasize data privacy and sustainability in underwriting real estate. They aim to protect consumers and the environment. Staying informed through industry updates prepares for compliance.

Read Also: Why Do Accountants Charge So Much? Exploring Accounting Firm CFO Services