Introduction

When embarking on the journey of purchasing a home, many buyers encounter various professionals who play essential roles in making the dream a reality. One such key figure is the underwriter, who can demystify a significant part of the transaction. We at numberfied are delighted to share this knowledge, as it empowers you to approach your real estate endeavors with confidence and clarity. The underwriter acts as a guardian of financial prudence, ensuring that loans are granted responsibly to mitigate risks for lenders and borrowers alike. This article provides comprehensive insights into their responsibilities, the processes they follow, and practical advice to help you succeed in your real estate goals. By understanding what an underwriter is in real estate, you can better prepare for the steps ahead, avoid common pitfalls, and foster a smoother experience.

Key Takeaways

- An underwriter evaluates loan applications to determine risk and eligibility.

- They thoroughly review financial documents, credit history, and property details.

- Understanding their role helps borrowers present stronger applications.

- The process typically takes several days to weeks, depending on complexity.

- Preparation and transparency are crucial for approval.

The Fundamentals of Underwriting in Real Estate

To fully appreciate what an underwriter in real estate is, it is essential to start with the basics of underwriting. This process involves a detailed assessment to ensure that a loan aligns with the lender’s guidelines and the borrower’s ability to repay. Knowledge of these fundamentals equips you to engage more effectively with the real estate market.

What Does an Underwriter Do?

An underwriter’s primary duty is to analyze the risk associated with extending a mortgage. They scrutinize every aspect of the application to confirm that it meets regulatory and institutional standards. This role requires a blend of analytical skills and attention to detail, ensuring that only viable loans proceed.

Qualifications and Skills Required for Underwriters

Underwriters typically hold degrees in finance, business, or related fields, often supplemented by certifications such as those from the Mortgage Bankers Association. Essential skills include proficiency in financial analysis, knowledge of real estate laws, and the ability to interpret complex data. We admire the dedication these professionals bring to their work, as it safeguards the integrity of real estate transactions.

Differences Between Underwriters and Other Real Estate Professionals

While loan officers originate mortgages and appraisers value properties, underwriters focus solely on risk assessment. Unlike agents who facilitate sales, underwriters operate behind the scenes to approve funding. Recognizing these distinctions clarifies what an underwriter in real estate is and how they fit into the broader ecosystem.

The Importance of Underwriters in Mortgage Approval

Underwriters serve as a critical checkpoint in the mortgage process, protecting both parties from potential financial distress. Their evaluations help maintain market stability by preventing over-lending. We are pleased to highlight that effective underwriting contributes to sustainable homeownership across the United States.

How Underwriters Mitigate Risks for Lenders

By verifying income, assets, and creditworthiness, underwriters reduce the likelihood of defaults. They employ sophisticated models to predict repayment probability, ensuring lenders’ portfolios remain healthy. Risk management is a cornerstone of what an underwriter does in real estate.

Impact on Borrowers Home Buying Experience

A thorough underwriting process can lead to conditional approvals, allowing buyers to address issues promptly. It ultimately fosters trust in the transaction, enabling borrowers to secure homes with favorable terms. Understanding this impact underscores the value of underwriters.

Regulatory Compliance and Ethical Considerations

Underwriters adhere to laws such as the Truth in Lending Act and the Fair Housing Act to promote fairness. Ethical practices ensure unbiased decisions, benefiting the entire real estate community. We encourage awareness of these standards to appreciate the professionalism involved.

The Mortgage Underwriting Process Explained

Delving deeper into what an underwriter is in real estate reveals the structured process they follow. This sequence transforms a loan application into an approved mortgage, involving multiple verification steps.

Initial Application Review

The process begins with examining the borrower’s submitted documents for completeness and accuracy. Underwriters flag any discrepancies early to streamline subsequent stages. This initial scrutiny sets the tone for efficient processing.

Document Verification and Analysis

Key documents such as tax returns, bank statements, and employment verifications are cross-checked. Advanced software helps detect fraud or inconsistencies. We find this step crucial for building a reliable financial profile.

Credit and Financial Assessment

Underwriters evaluate credit scores, debt-to-income ratios, and payment histories. They consider factors like recent inquiries or derogatory marks. A comprehensive assessment ensures the borrower’s financial stability aligns with loan requirements.

Property Appraisal and Valuation

An independent appraisal confirms the property’s worth matches the loan amount. Underwriters review this report to avoid overvaluation risks. This integration of property data is integral to what an underwriter is in real estate.

Conditional Approval and Final Decision

If initial reviews are positive, conditional approvals may be issued, requiring additional information. Once all conditions are met, final approval is granted. This phased approach minimizes surprises for borrowers.

Timeline and Potential Delays

The underwriting timeline ranges from 1 to 4 weeks, depending on application volume and complexity. Delays can arise from incomplete documentation or external verifications. We advise patience and proactive communication to expedite the process.

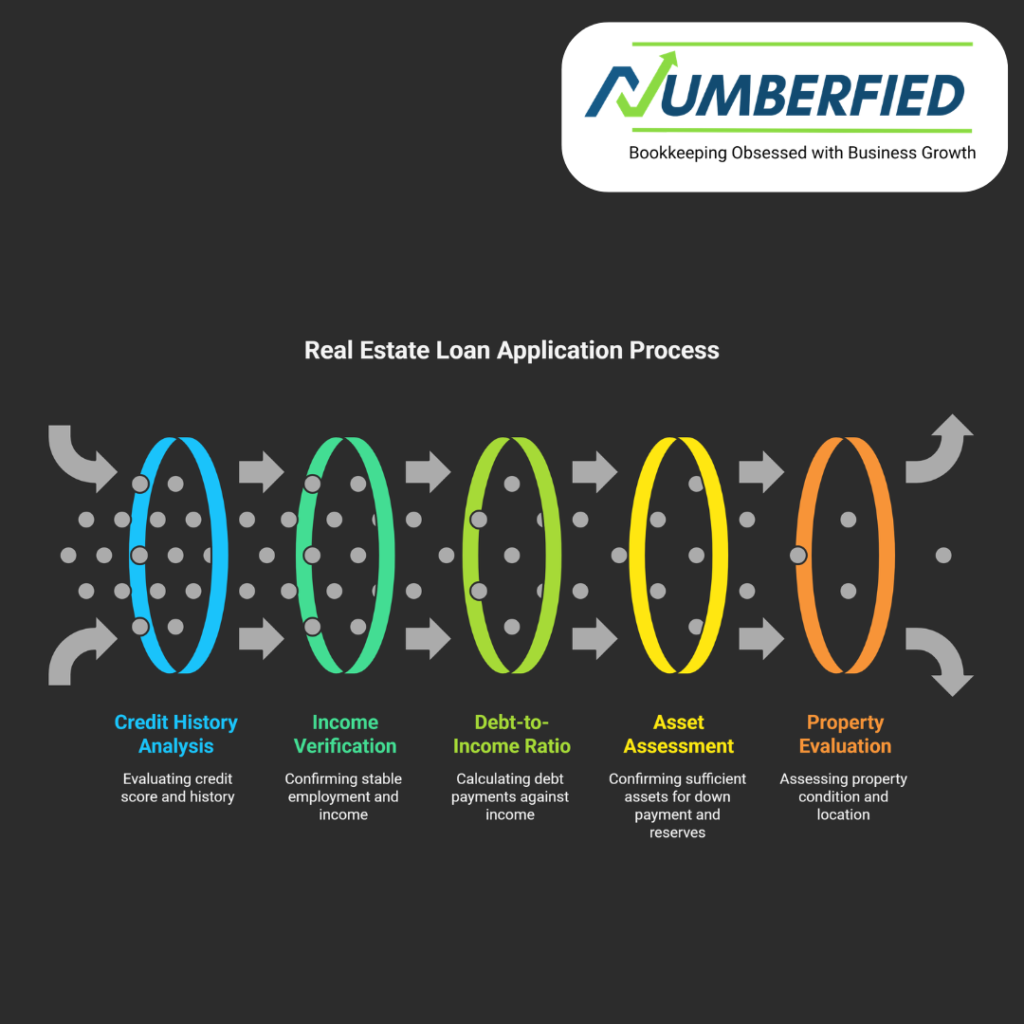

Key Factors Underwriters Evaluate in Applications

Understanding what an underwriter in real estate involves knowing the specific criteria they prioritize. These factors form the basis of their decisions, ensuring loans are sustainable.

Credit History and Score Analysis

A strong credit score above 700 often facilitates approval, while lower scores may require explanations. Underwriters look for patterns of responsible credit use. Improving your score beforehand can enhance your application’s appeal.

Income and Employment Verification

Stable employment for at least two years and verifiable income sources are essential. Self-employed borrowers may need additional tax documentation. We recommend organizing these records meticulously.

Debt-to-Income Ratio Calculations

This ratio compares monthly debt payments to gross income and ideally is below 43%. High ratios signal potential repayment challenges. Managing debts effectively can improve this metric.

Asset and Reserve Requirements

Underwriters confirm that sufficient assets are available for down payments and reserves for several months’ expenses. Liquid assets, such as savings accounts, are preferred. Building reserves demonstrates financial preparedness.

Property-Specific Considerations

The property’s condition, location, and type influence approval. Issues like environmental hazards may necessitate further inspections. Aligning property choices with underwriting standards is advisable.

Risk Assessment Models Used

Underwriters employ automated systems and manual reviews to gauge overall risk. These models incorporate economic trends and borrower profiles. Familiarity with these tools highlights the sophistication of what an underwriter is in real estate.

Common Challenges Faced During Underwriting

Even with preparation, challenges can arise in the underwriting process. Recognizing these allows borrowers to anticipate and address them effectively.

Incomplete or Inaccurate Documentation

Missing forms or errors in submissions are frequent hurdles. Underwriters require precise information to proceed. Double-checking applications prevents unnecessary setbacks.

Credit Issues and How to Resolve Them

Disputes on credit reports or high utilization can complicate approvals. Obtaining credit reports in advance and correcting errors is beneficial. We suggest monitoring credit regularly.

Employment Changes During the Process

Job switches mid-process may trigger re-verification, potentially delaying approval. Stable employment is ideal during underwriting. Communicating changes promptly helps manage expectations.

Appraisal Discrepancies

If the appraisal value falls short of the purchase price, renegotiation or additional funds may be needed. Choosing comparable properties wisely aids in accurate valuations.

Economic Factors Influencing Decisions

Market fluctuations, interest rate changes, or economic downturns can affect underwriting stringency. Staying informed about trends helps improve application timing.

Overcoming Denials and Appeals

If denied, underwriters provide reasons, allowing for corrections in resubmissions. Appeals involve presenting new evidence. Persistence and improvement can lead to eventual success.

Tips for Borrowers to Prepare for Underwriting

To make the most of what an underwriter is in real estate, preparation is key. These tips empower you to present a compelling application.

Organizing Financial Documents Effectively

Compile pay stubs, tax returns, and bank statements in advance. Digital organization tools can streamline submission. This readiness impresses underwriters and accelerates reviews.

Improving Creditworthiness Before Applying

Pay down debts, avoid new credit, and dispute inaccuracies. Consistent on-time payments build a positive history. We encourage starting this process months ahead.

Understanding Lender Guidelines

Research specific lender requirements, as they vary. Conventional, FHA, and VA loans have distinct criteria. Aligning with these enhances approval chances.

Communicating with Your Loan Officer

Maintain open dialogue for updates and clarifications. They can guide you through underwriter requests. This collaboration fosters a positive experience.

Avoiding Major Financial Changes

Refrain from making large purchases or opening new accounts during underwriting. Such actions can adversely affect your financial profile. Stability is paramount.

Seeking Professional Advice When Needed

Consult financial advisors or real estate experts for complex situations. Their insights can refine your approach. We at numberfied are here to offer general guidance on these matters.

The Evolution of Underwriting in Real Estate

As the industry advances, so does the role of the underwriter in real estate. Emerging trends are reshaping this essential function.

Technological Advancements in Underwriting

Automated systems and AI accelerate document analysis and risk prediction. These tools enhance accuracy and efficiency. We are excited about how technology streamlines processes for everyone.

Impact of Digital Tools and AI

Machine learning identifies patterns in data, reducing human error. Digital platforms facilitate faster verifications. This evolution makes underwriting more accessible.

Regulatory Changes and Their Effects

Updates to laws like Dodd-Frank influence underwriting standards. Stricter regulations promote transparency. Staying abreast of changes ensures compliance.

Sustainability and Green Underwriting Practices

Underwriters increasingly consider energy-efficient properties for favorable terms. This shift supports environmental goals. We appreciate this forward-thinking approach.

Global Influences on U.S. Real Estate Underwriting

International economic trends affect domestic lending. Trade policies and global events can tighten criteria. Awareness of these factors aids strategic planning.

Future Predictions for the Role of Underwriters

We anticipate greater integration of data analytics and remote processes. Underwriters may focus more on advisory roles. This progression promises even more efficient real estate transactions.

Conclusion

In summary, grasping what an underwriter in real estate is illuminates a pivotal aspect of the home-buying journey. From assessing risks to ensuring compliance, underwriters uphold the foundation of secure mortgages, benefiting borrowers and lenders nationwide. Key takeaways include the importance of thorough preparation, understanding evaluation factors, and navigating challenges with resilience. As we at numberfied continue to support informed real estate decisions, we invite you to connect with us for personalized insights. Whether you have questions about the process or need guidance, reaching out can make your path smoother. Contact numberfied today to discuss how we can assist in your real estate endeavors.

FAQs

How long does the underwriting process typically take in real estate?

The underwriting process usually spans 1 to 4 weeks, depending on the application’s complexity and the lender’s workload. Factors like document completeness and external verifications influence the timeline. Borrowers can help by submitting accurate information promptly to avoid delays.

Can I appeal a mortgage underwriting denial?

Yes, you can appeal a denial by providing additional documentation or explanations to address the underwriter’s concerns. Lenders often outline the appeal process in their denial letter. Working closely with your loan officer increases the chances of a successful reconsideration.

What documents are most important for underwriters to review?

Essential documents include recent pay stubs, tax returns for the past two years, and bank statements. Employment verification and credit reports are also critical. Organizing these clearly demonstrates your financial reliability to the underwriter.

How does an underwriter determine my debt-to-income ratio?

Underwriters calculate this by dividing your total monthly debt payments by your gross monthly income. They aim for a ratio below 43% for most loans. Lowering existing debts before applying can improve this key metric.

What role does property location play in underwriting?

Location affects risk assessment through factors such as market stability, flood zones, and economic conditions. Underwriters review comparable sales and potential hazards. Choosing properties in stable areas can facilitate smoother approvals.

Are there different types of underwriters in real estate?

Yes, including manual underwriters who handle complex cases and automated systems for straightforward applications. Some specialize in government-backed loans, such as FHA or VA. Each type has specific guidelines for evaluating eligibility.

How can I track the status of my underwriting?

Communicate regularly with your loan officer, who can provide updates from the underwriter. Many lenders offer online portals for real-time tracking. Staying informed helps you respond quickly to any requests.

What happens if my appraisal comes in lower than expected?

Underwriters may require price renegotiation, additional down payment, or loan denial if the value gap is significant. You can challenge the appraisal with evidence of comparable properties. Addressing this promptly is essential for proceeding.

Do underwriters consider my savings reserves?

Yes, they verify reserves to ensure you can cover mortgage payments for several months if needed. Typically, two to six months’ worth is ideal. Building these reserves strengthens your application profile.

How has remote work affected real estate underwriting?

Remote work has led underwriters to scrutinize income stability more closely, especially for self-employed or gig economy borrowers. They may request additional proof of consistent earnings. Adapting documentation to reflect remote setups can aid approval.

Read Also: Why Do Accountants Charge So Much? Exploring Accounting Firm CFO Services